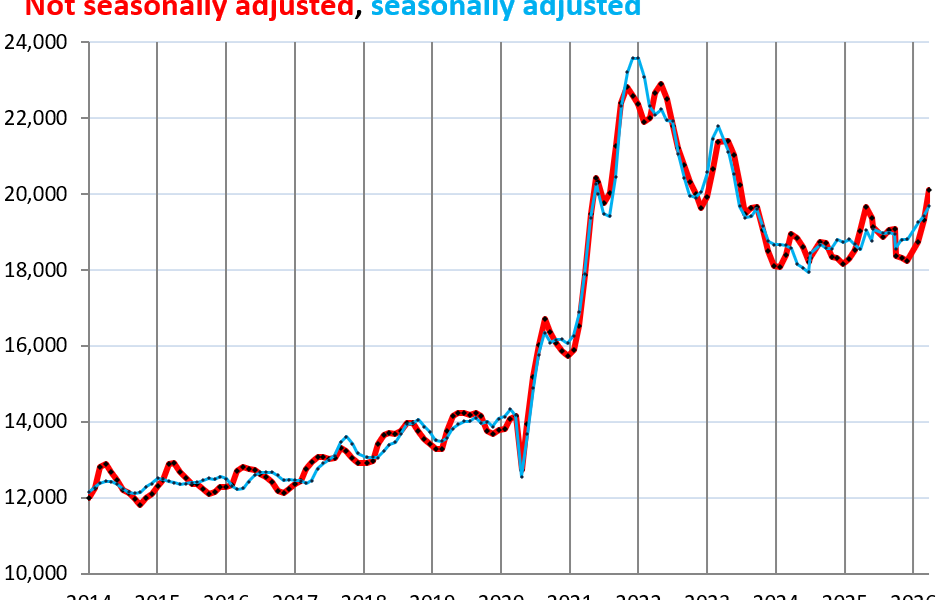

Wholesale prices for used vehicles surged 4.2% in March from February, not seasonally adjusted, hitting $20,102 per unit. That’s the sharpest monthly jump since the pandemic-era spike that kicked off broad inflation in 2020. Year-over-year, prices rose 5.7%. Seasonally adjusted, the Manheim Used Vehicle Value Index (MUVVI) climbed 1.4% month-over-month. Manheim, the biggest U.S. auto auction operator under Cox Automotive, tracks these dealer-to-dealer sales, which signal retail trends ahead of time.

Dealers drove the bidding frenzy. They see empty lots and strong retail demand, so they paid up confidently, expecting to pass costs to buyers. Sales conversion rates at auctions hit 68.2%—4.6 points above the three-year March average and 5.5 points higher than February’s 62.7%. Supply stays tight from rental fleets dumping old cars, finance companies selling off-leases and repos, plus corporate and government vehicles. Cox calls demand “healthy,” pinned on fat tax refunds acting as down payments.

IRS data through March 27 shows total refunds up 13.6% year-over-year, averaging $3,521 per filer—a 11.1% increase. Lawmakers baked this into the “One, Big, Beautiful Bill Act” (OBBB), rammed through in July 2025 to juice the economy pre-midterms. Bigger refunds mean more cash for cars, but they also drain Treasury coffers and stoke demand without matching supply. Used vehicles fit the bill: affordable transport amid high new-car prices.

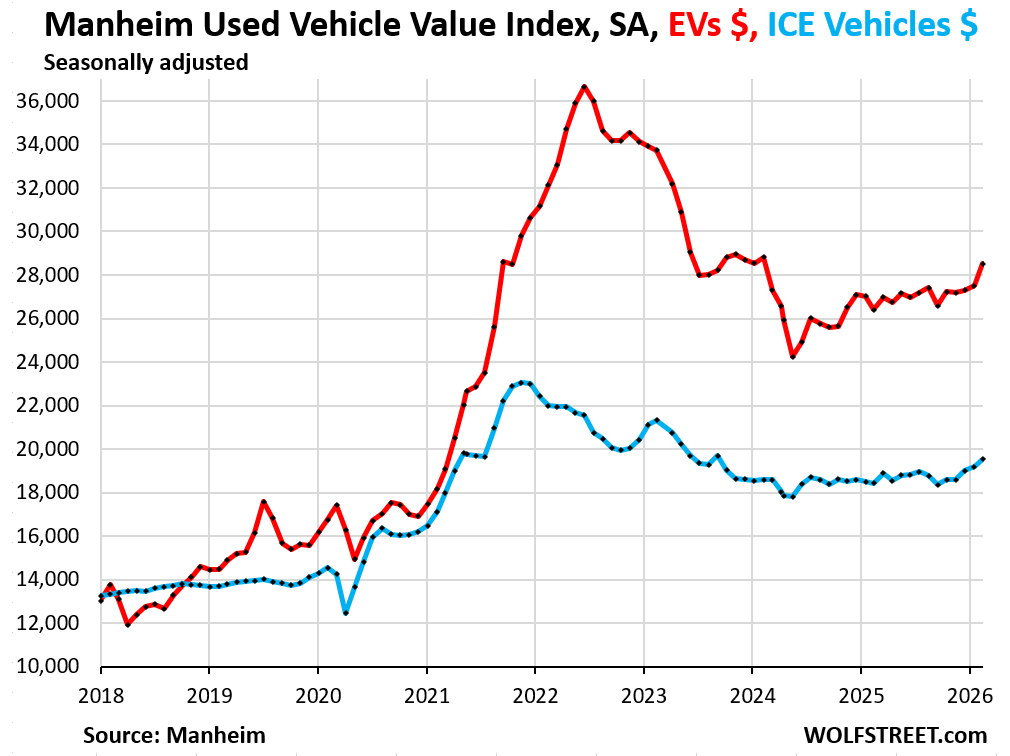

Electric Vehicles Outpace Gas Cars

EVs led the charge. Wholesale prices jumped 3.7% month-over-month seasonally adjusted and 8.0% year-over-year to $28,471. Gas-powered (ICE) vehicles rose 1.8% monthly and 4.2% annually to $19,874. Cox notes EVs beat expectations in Q1, with record wholesale volume of nearly 37,000 units. Off-lease returns flooded auctions, boosting availability.

Retail used EV sales topped 100,000 in Q1—second-best quarter ever, trailing only Q3 of some prior year (data cuts off there). Rising gas prices likely helped: dealers snapped up used EVs, cheaper than new ones starting at $40,000-plus after incentives. But skepticism creeps in. EV demand feels propped by subsidies and cheap leases cycling back. True organic pull? Gas at $3.50/gallon nationally tests that.

Why This Signals Broader Inflation Risks

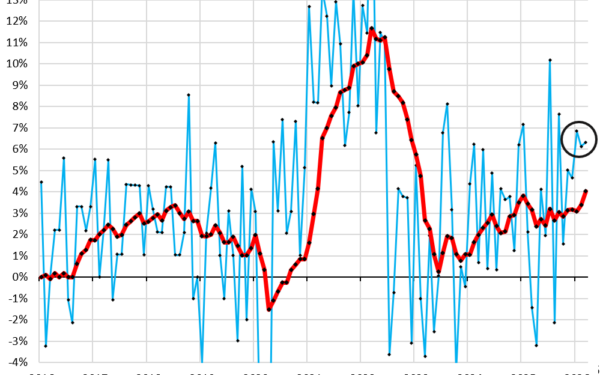

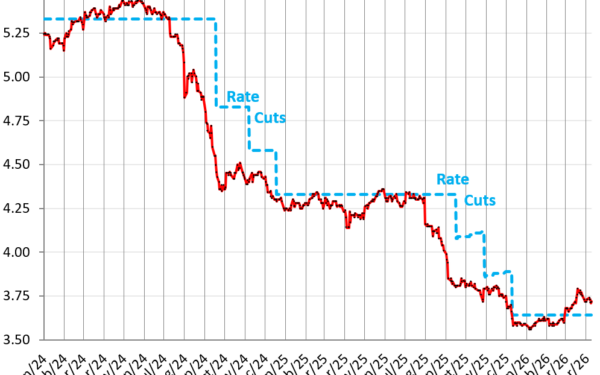

Used cars ignited CPI inflation in 2020-2022, peaking at 45% year-over-year in 2021. Wholesale spikes precede retail by 1-2 months; expect sticker prices to follow. If auctions stay hot, vehicle CPI—10% of the index—could add 0.2-0.4 points to headline inflation monthly. Fed watches this closely; rate cuts hinge on cooling pressures.

Context matters. New vehicle production lags at 15.5 million annualized (March data), down from 17 million pre-COVID norms due to chips, strikes, and EV mandates. Inventories sit at 2.8 months’ supply for used cars versus 3.5 ideal. Tax refunds add $30 billion extra liquidity, per IRS pace, hitting an economy already at 2.5% GDP growth Q1 estimates.

Fair take: This isn’t 2020 redux yet—no chip shortages or lockdowns. But pipelines don’t lie. Dealers won’t eat margins forever; consumers face 7% auto loans. If gas climbs to $4, EV flips could accelerate, but ICE dominance (95% sales) keeps pressure broad. Watch April auctions. Sustained 2%+ monthly gains? Inflation narrative flips hard. Bond yields tick up, stocks wobble. Households budget tighter. That’s the pipeline pressure building.