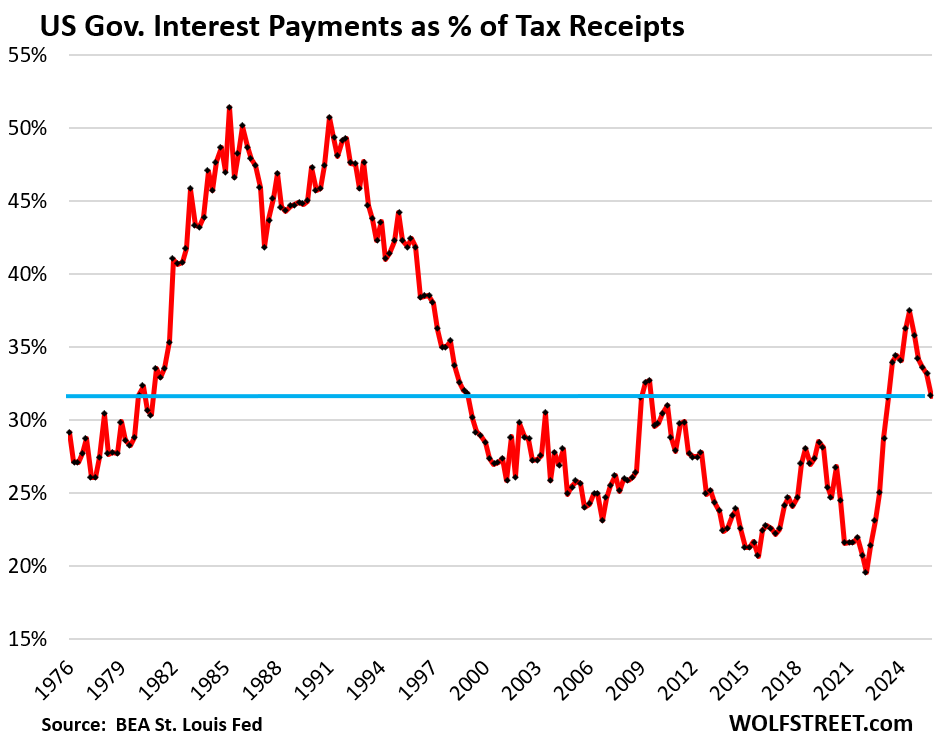

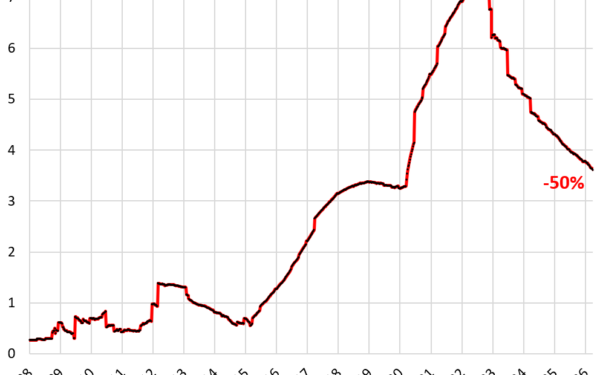

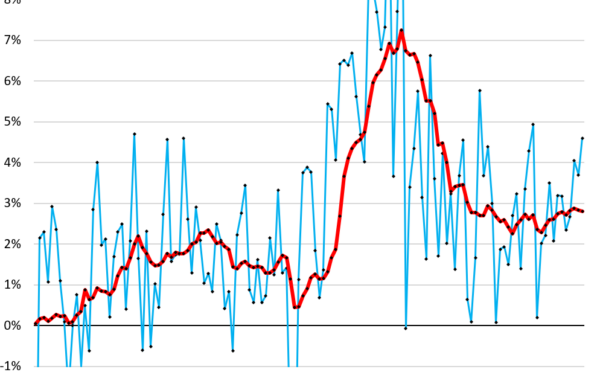

In Q4 2025, US federal interest payments consumed 31.6% of tax receipts available for general budget spending. This marks an improvement from the 37.5% peak in Q3 2024—the worst since 1996—but signals persistent fiscal strain. Tax receipts hit a quarterly record of $902 billion, up 7.4% from Q3. Annual receipts reached $3.57 trillion, a 14.6% jump. Interest expenses climbed to $307 billion, up just 2.4% quarter-over-quarter. These figures come from the Bureau of Economic Analysis’s revised National Accounts data.

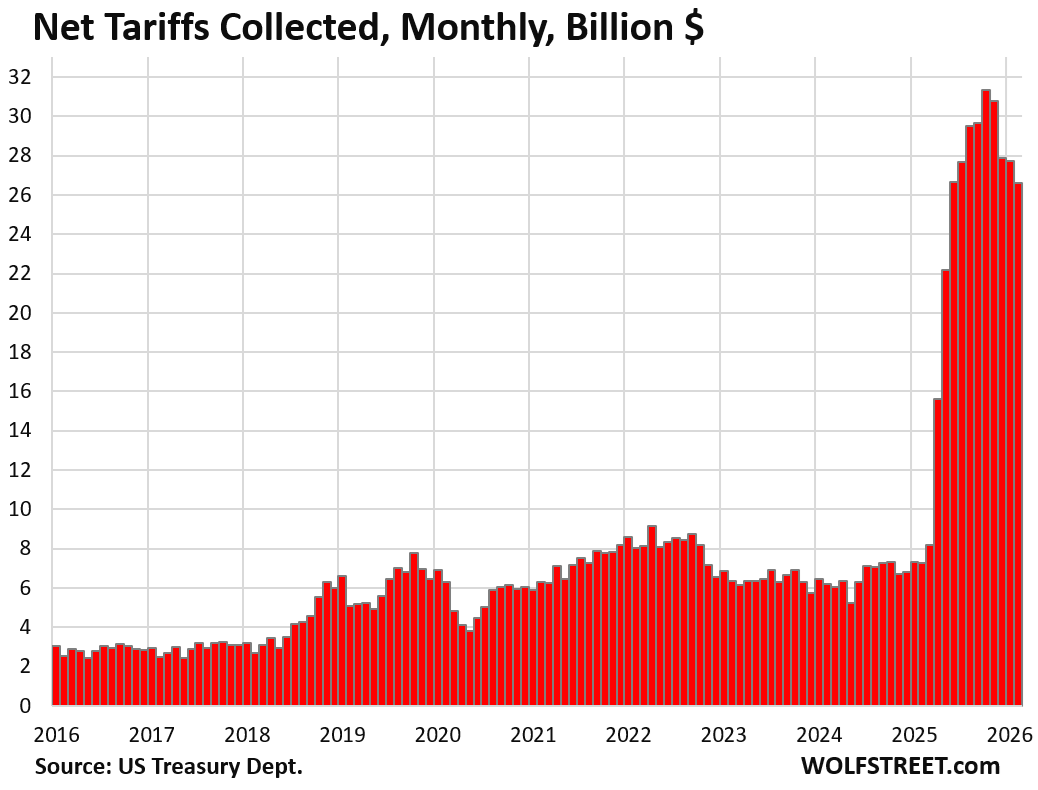

Tax receipts exclude Social Security and disability contributions, which fund trust funds outside the general budget. A growing economy drove the gains: higher taxable income from corporations and individuals, plus capital gains taxes from rising asset prices. Tariffs added $90 billion in Q4 alone, pushing past-12-months totals to $304 billion through February 2026. But the Supreme Court invalidated parts of these tariffs, triggering refunds. Replacement tariffs under new laws are in place, yet net collections will likely shrink in 2026. Capital gains taxes remain volatile—2022’s asset plunge proved that.

Debt Servicing Costs Stabilize Amid Higher Rates

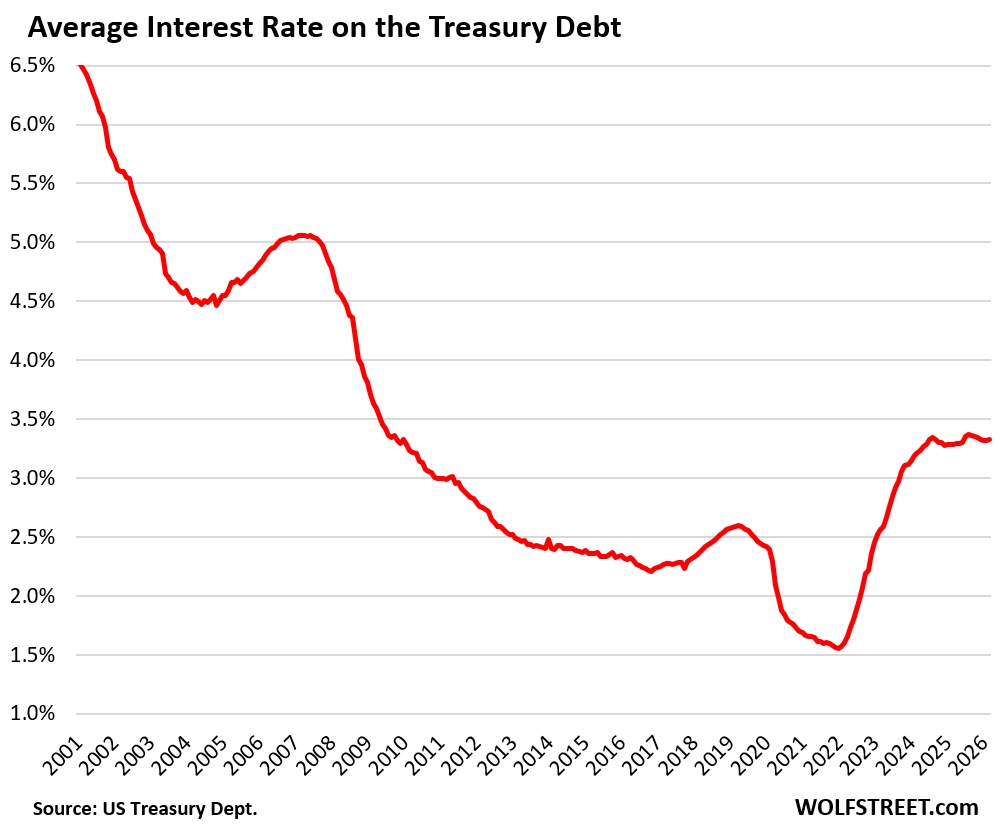

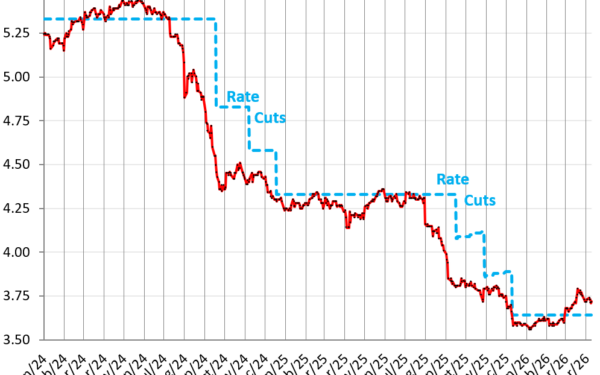

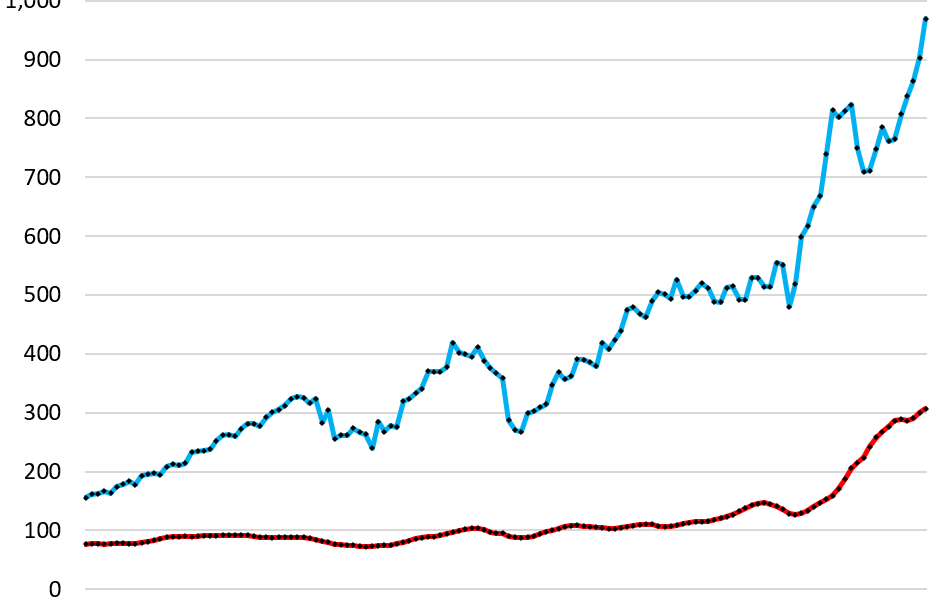

The average interest rate on Treasury debt held steady at 3.33% in March 2026, per Treasury data, after fluctuating between 3.30% and 3.37% since Q3 2024. This follows a doubling since the Fed’s first rate hikes in early 2022. New debt rolls over at these elevated rates: maturing securities get replaced, and deficit funding adds fresh issuance. Short-term Treasury bills total $6.8 trillion, exposing the government to refinancing risk if rates spike.

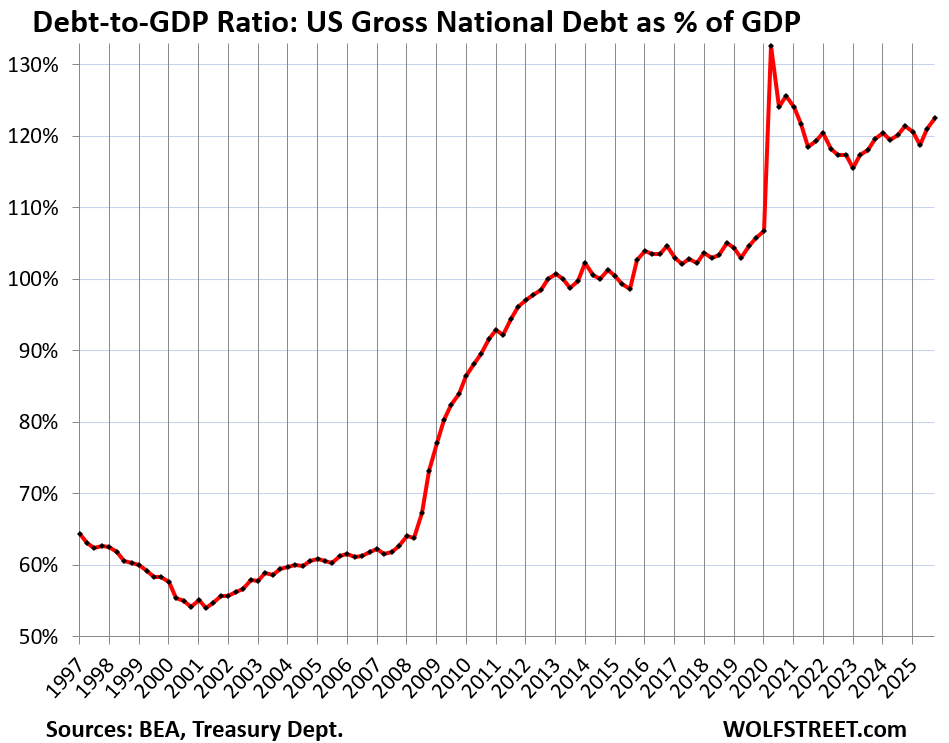

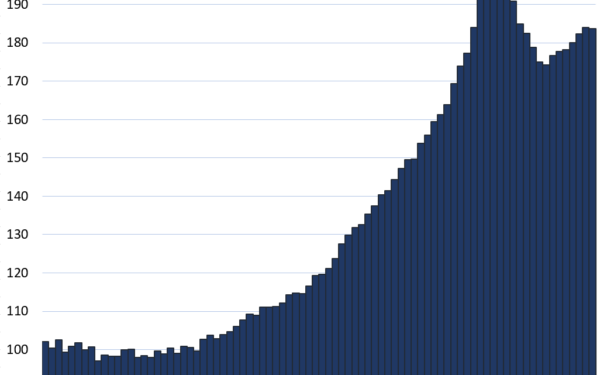

Total public debt exceeds $36 trillion, with gross debt around $37 trillion including intragovernmental holdings. The debt-to-GDP ratio climbed to approximately 128% in Q4 2025, up from 122% in 2023 and 100% a decade ago. Projections from the Congressional Budget Office peg it at 166% by 2054 under current policies, assuming no recessions or wars. Persistent deficits—$1.8 trillion in FY 2025—fuel the rise, as spending outpaces revenues despite tariff boosts.

Why This Matters: Crowding Out and Systemic Risks

Interest payments now rival defense spending ($816 billion in FY 2025) and exceed Medicare. At 31.6% of general tax receipts, they leave less for salaries, infrastructure, or discretionary programs. Lawmakers face stark choices: raise taxes, slash spending, or print money via the Fed—each risks backlash or inflation. Higher debt service already crowds out private investment; yields on 10-year Treasuries hover near 4.5%, pressuring mortgages and corporate borrowing.

Skeptically, the “less ugly” narrative ignores structural flaws. Demographic shifts boost entitlement costs, while political gridlock blocks reforms. If rates rise to 5%—plausible with inflation or safe-haven demand—the annual interest bill could hit $1.8 trillion, devouring half of tax receipts. Investors should watch: foreign holders like Japan and China own $8 trillion combined, and diversification away from USD assets accelerates.

For crypto holders, this underscores Bitcoin’s appeal as a non-sovereign store of value. US fiscal math doesn’t add up long-term; debt monetization erodes fiat purchasing power. Yet Treasuries remain the global benchmark—until they don’t. Track the Monthly Treasury Statement for real-time receipts and outlays; deficits won’t vanish without pain.