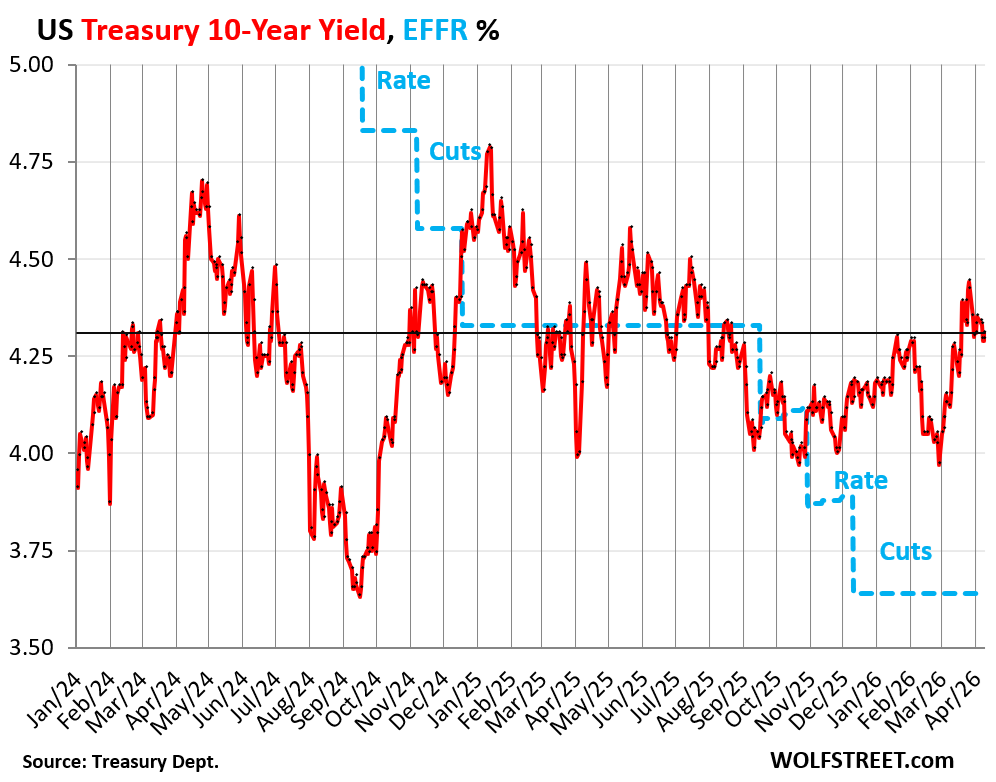

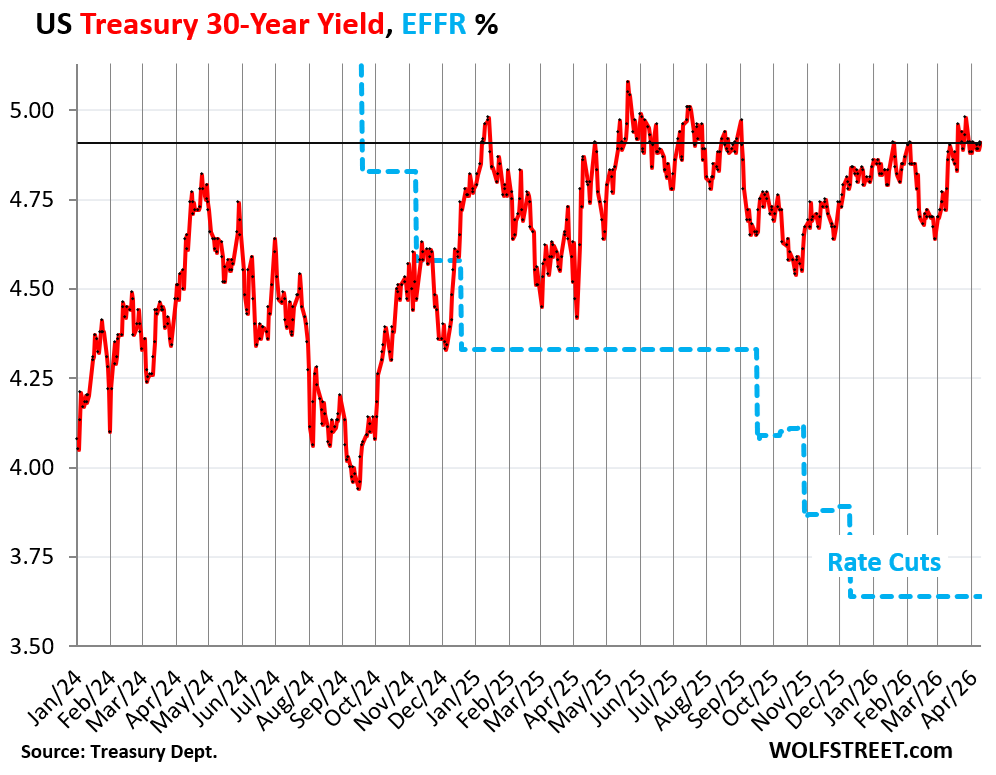

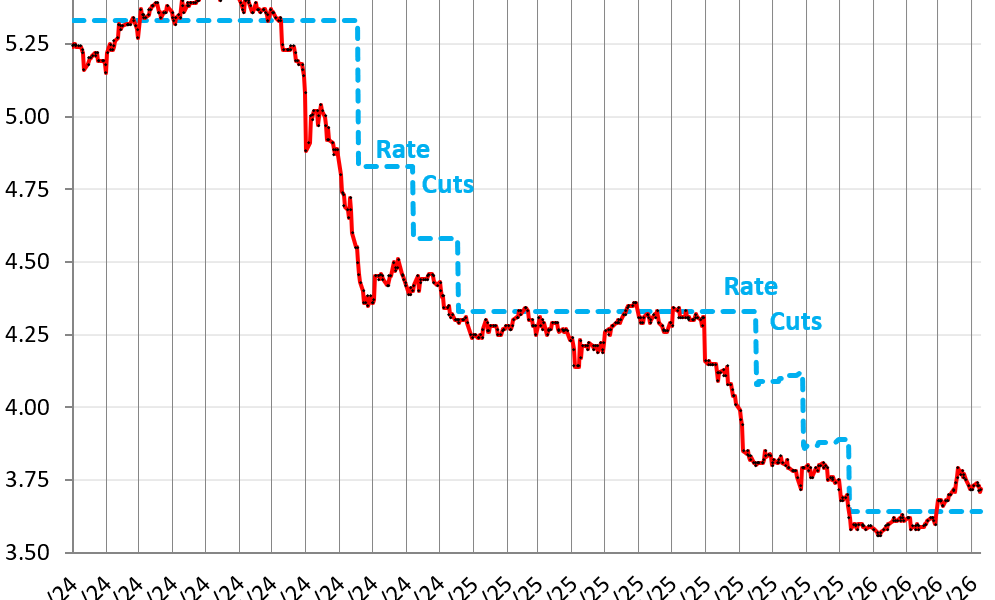

The US Treasury offloaded $620 billion in securities this week across nine auctions—$480 billion in bills and $140 billion in notes and bonds. The 10-year yield closed Friday at 4.31%, the 30-year at 4.91%. These levels look complacent amid surging deficits, record issuance, and inflation that refuses to fade below 3% core PCE. Markets bet on Fed rate cuts despite the supply glut. That could backfire.

Tax season cushioned the blow. April inflows from Q1 estimates and capital gains taxes let Treasury shrink three short-term bill auctions by $55 billion versus March and $65 billion versus February. Still, bills dominated: 4-week at 3.56%, 6-week 3.615%, 8-week 3.575%, up to 52-week at 3.615%. The 26-week auction yield jumped 8 basis points from last week to 3.615%, matching an investment rate of 3.73%.

Auction Breakdown - Bills ($480B total):

4-week (Apr 9): $81B, 3.560%

6-week (Apr 7): $75B, 3.615%

8-week (Apr 9): $76B, 3.575%

13-week (Apr 6): $96B, 3.635%

17-week (Apr 8): $70B, 3.600%

26-week (Apr 6): $83B, 3.615%

52-week (Apr 11?): Remaining balance

Short-end yields now exceed the Fed’s 5.33% effective funds rate—3-month closed at 3.71%, 6-month around 3.73%. This inversion signals markets doubt near-term cuts, or worse, price in hikes if inflation reignites. Back in March, 6-month yields first broke above EFFR amid geopolitical jitters; that gap persists.

Notes and Bonds: Supply Meets Skeptical Buyers

Longer maturities fetched $140 billion: $68 billion 3-year notes at 3.897%, $46 billion 10-year at 4.282% (up 6 bps from March), $26 billion 30-year bonds at 4.876%. Secondary market pushed 10-year to 4.32% by Friday, 30-year near 4.91%. This week’s 10-year auction refinanced $20 billion maturing from 2016’s 1.765% vintage, net adding $26 billion outstanding.

Notes & Bonds ($140B):

3-year (Apr 7): $68B, 3.897%

10-year (Apr 8): $46B, 4.282%

30-year (Apr 9): $26B, 4.876%

Outstanding 10-year notes swelled accordingly. Total marketable Treasuries top $27 trillion, with quarterly issuance routinely exceeding $1 trillion to fund $1.8 trillion FY2024 deficits—projected to hit $2 trillion annually soon. Primary dealers absorbed much of this week’s supply, but tails widened slightly, hinting at buyer fatigue.

Why Yields Stay Stubbornly Low—and Why It Matters

Markets fixate on Fed dots forecasting three 2024 cuts to 4.6% funds rate, ignoring fiscal reality. Core PCE lingers at 2.8%, but shelter costs and sticky services keep it above 3% in spots. Fed Chair Powell signals tolerance for 3%+ if jobs hold—echoing 2021’s “transitory” misstep. A fresh inflation wave from supply shocks or wage spirals could force yields higher fast.

Implications cut deep. Every 10-year yield tick above 4.5% adds billions to interest costs, now $870 billion yearly, rivaling defense spending. Mortgages hover at 7%, crimping housing. Stocks ignore this—S&P up 10% YTD—but bond vigilantes lurk. If China dumps holdings (down $100B+ since 2022) or foreigners balk, auctions falter.

Skeptically, yields aren’t “too low” yet; they’ve doubled from 2020 lows. But pricing 100 bps cuts by year-end amid 5% deficits-to-GDP? That’s optimism bordering on denial. Watch May auctions: if tails blow out or yields spike 20 bps, the tantrum restarts. Investors, front-run the math—supply drowns demand unless inflation craters or deficits shrink. Neither looks likely.