Foreign holdings of US Treasury securities hit a record $9.49 trillion in February 2026, up $198 billion from January and $587 billion over the past year. This surge props up demand for the US government’s $39 trillion debt pile. But dig deeper: much of this “foreign” buying comes from US hedge funds parked in the Cayman Islands running the basis trade, and Corporate America routing through Ireland to skirt taxes. True outsider appetite looks shakier.

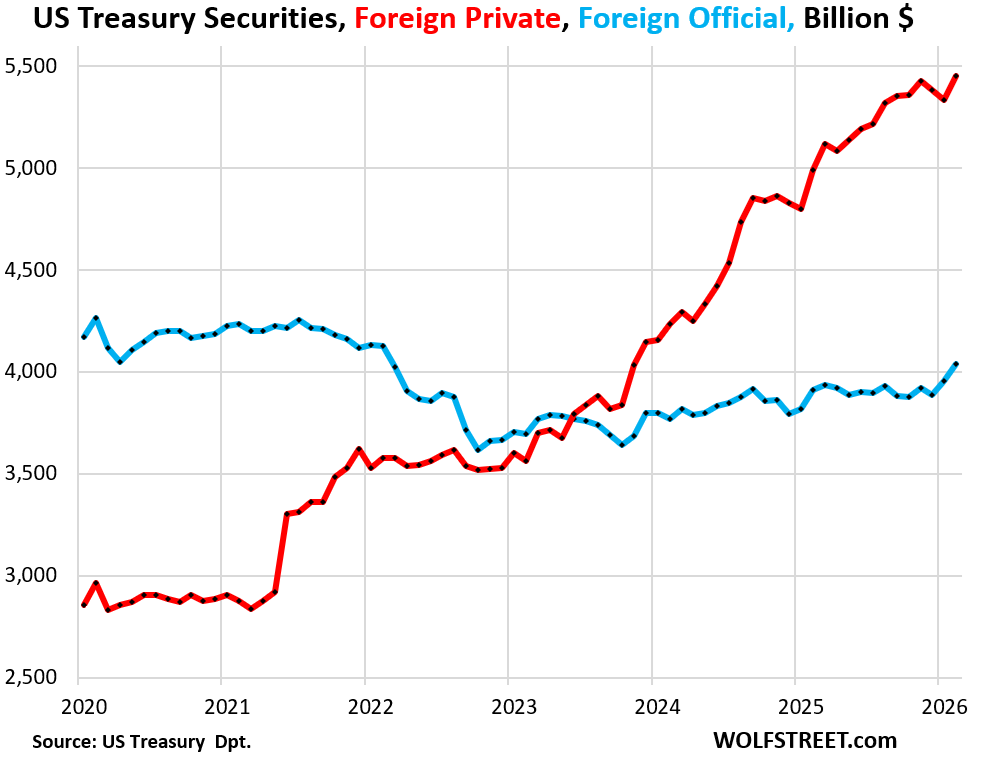

Private foreign investors drove the action, adding $117 billion in February to reach $5.45 trillion—a new high. These include overseas funds, companies, and individuals, but also plenty of disguised US players. Official holders like central banks piled on $81 billion that month, hitting $4.04 trillion total. That’s up $126 billion yearly but still below peaks from a few years back.

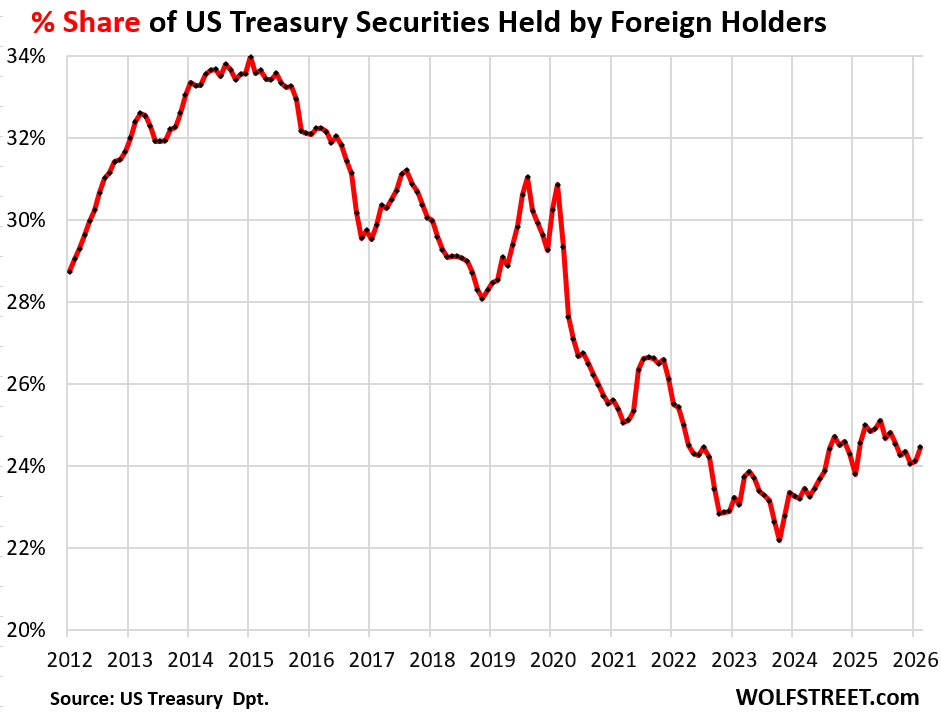

Foreign share of outstanding Treasuries climbed to 24.5% in February, the highest since September 2025. It peaked at 34% in 2015, dipped to 22% in late 2023, then rebounded. During the 2025 debt ceiling standoff, debt issuance stalled while foreigners kept buying, boosting their slice. Post-July, massive issuance resumed to cover deficits and refill the Treasury’s cash drawer, tempering the share gain.

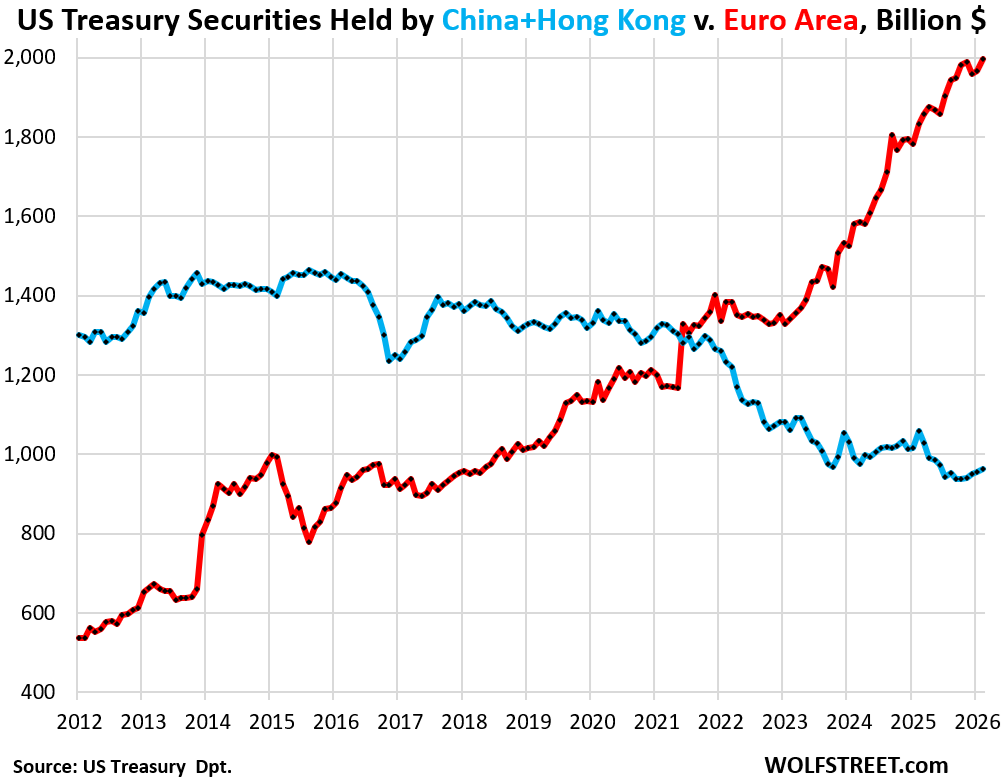

China Dumps, Europe Loads Up

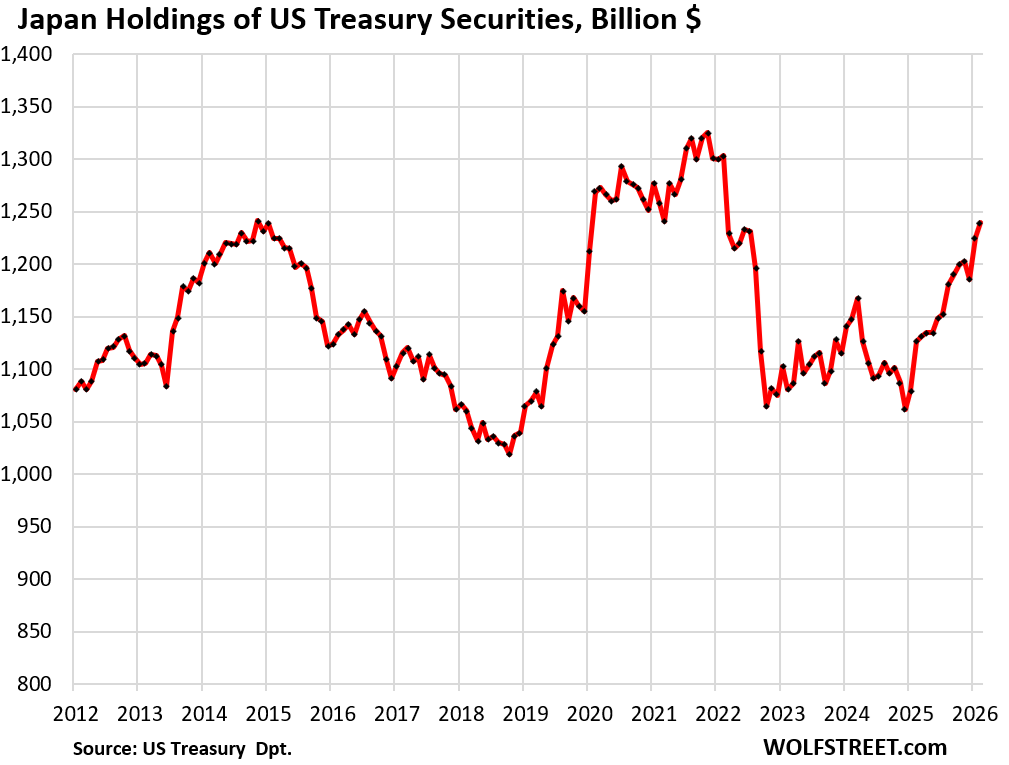

China and Hong Kong together shed over one-third of their holdings in the last decade, dropping $96 billion in the past year to $962 billion. They added just $8 billion in February. Geopolitical tensions, yuan support needs, and diversification explain the retreat. Meanwhile, the Euro Area went on a spree, adding $32 billion in February to a record around $2 trillion. Japan holds steady at about $1.1 trillion, the top single-country holder.

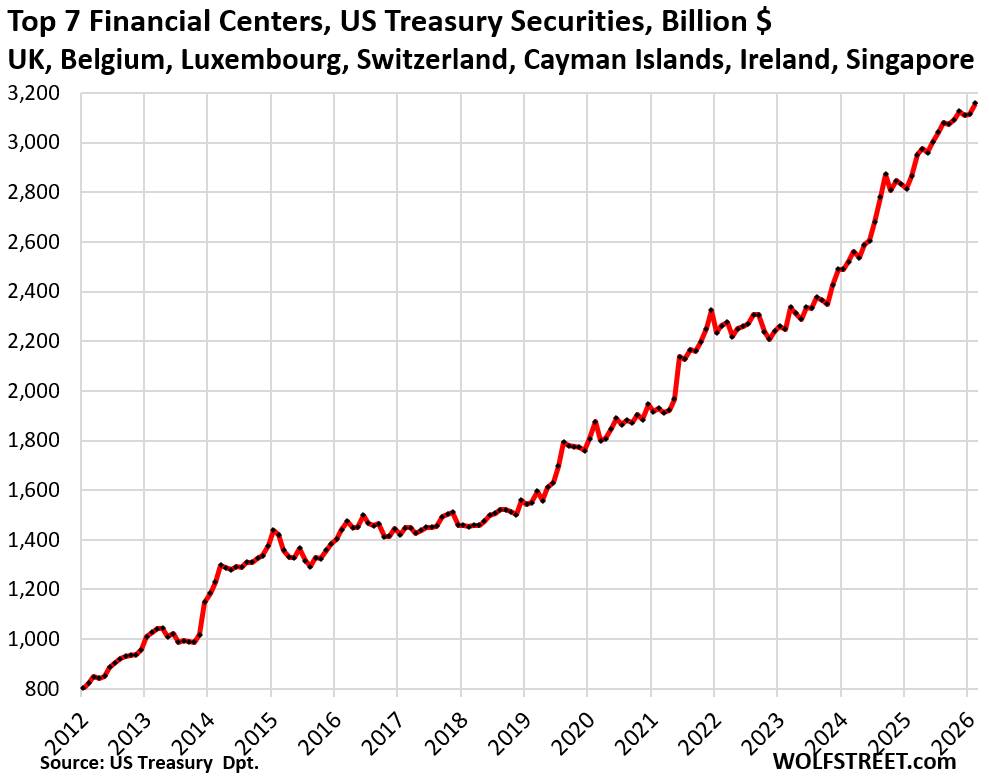

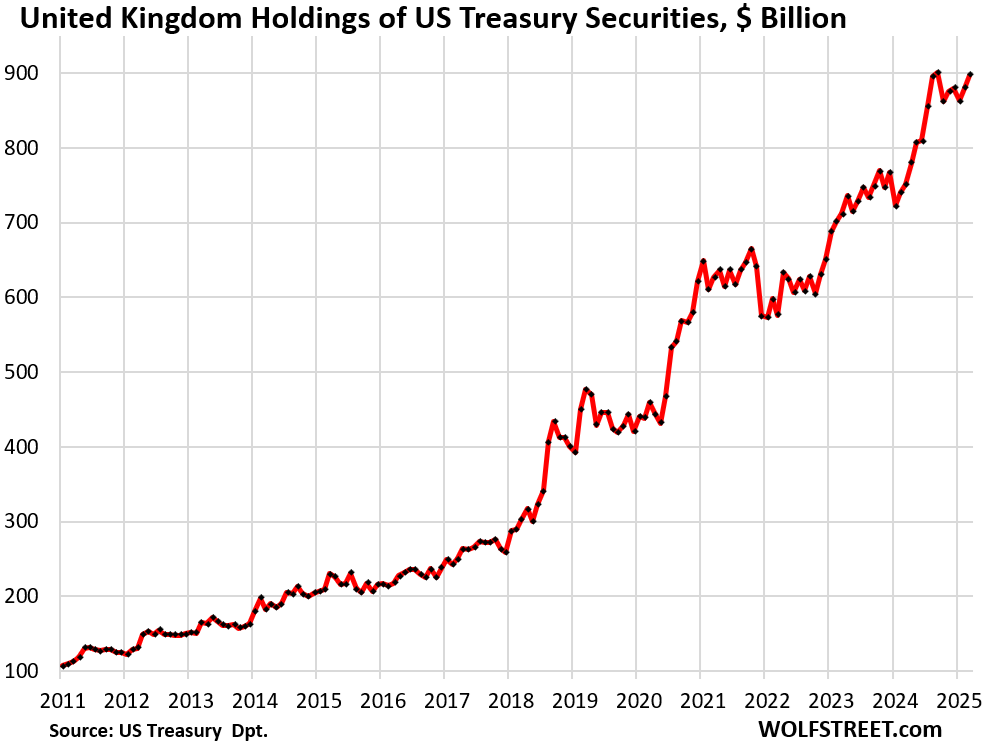

Other big players: UK at $807 billion (up recently, likely City of London funds), Belgium at $377 billion (Euroclear custody hub), and Cayman Islands at $340 billion—pure basis trade territory. Ireland’s $310 billion flags tech giants’ tax maneuvers.

The Basis Trade’s Hidden Leverage

The basis trade exploits the spread between Treasury cash prices and futures. Hedge funds buy Treasuries with cheap repo financing, sell equivalent futures, pocketing the “basis” difference. Leverage amplifies returns: funds borrow 50-100x against collateral. Cayman domiciliation lets them count as “foreign” in Treasury data, inflating official numbers.

Estimates peg basis trade exposure at $800 billion to $1 trillion in Treasuries as of early 2026, per Fed and analyst reports. It grew post-2020 volatility when repo markets seized. Unwind risks loom: a spike in repo rates or margin calls could force mass selling, as in March 2020 when basis trades amplified Treasury market chaos.

Why does this matter? It masks weak genuine foreign demand. Central banks like China’s are net sellers amid reserve shifts to gold and alternatives. If basis traders pull back—say, from Fed rate cuts disrupting repo or regulatory scrutiny—yields could jump 50-100 basis points fast. That adds billions to US interest costs, now over $1 trillion annually, fueling deficits projected at $2 trillion yearly by 2027.

Skeptically, Treasury data offers a veneer of stability. Strip out offshore US games, and foreign take-up barely covers new issuance. Europe fills the China void, but for how long? ECB balance sheet pressures and EU fiscal woes could reverse flows. Investors watch these numbers for yield signals: sustained records buy time for policymakers, but leverage beneath threatens a rude awakening.

Bottom line: US debt sustainability hinges on this illusion of demand. Real appetite from abroad stays tepid; domestic shadows prop it up. A basis trade stumble or official dumper could spike 10-year yields past 5%, hammering budgets and markets.