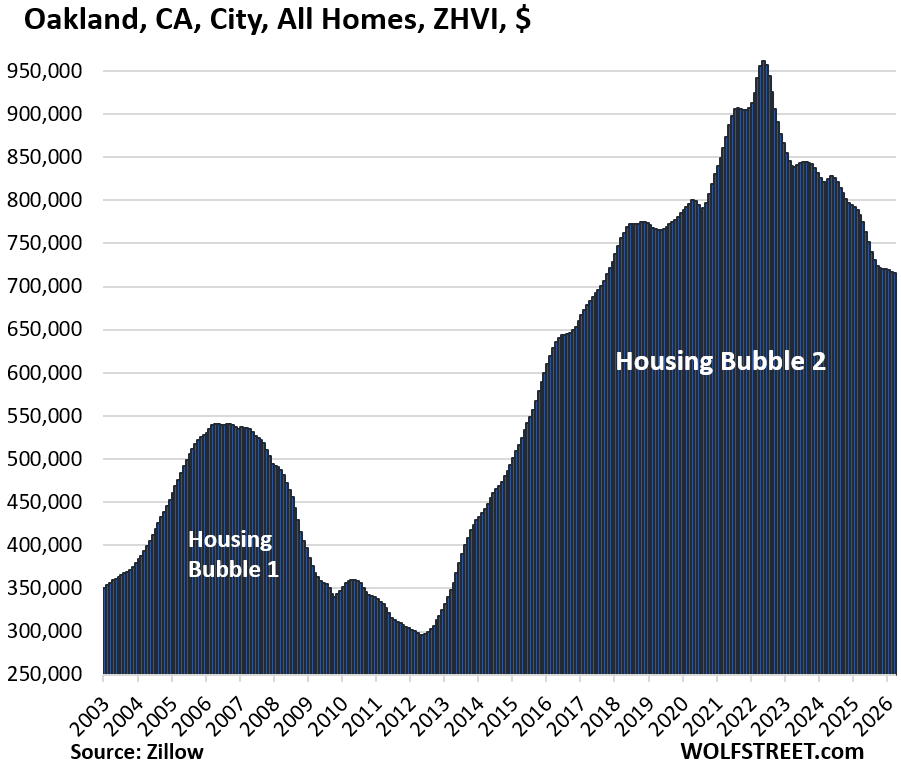

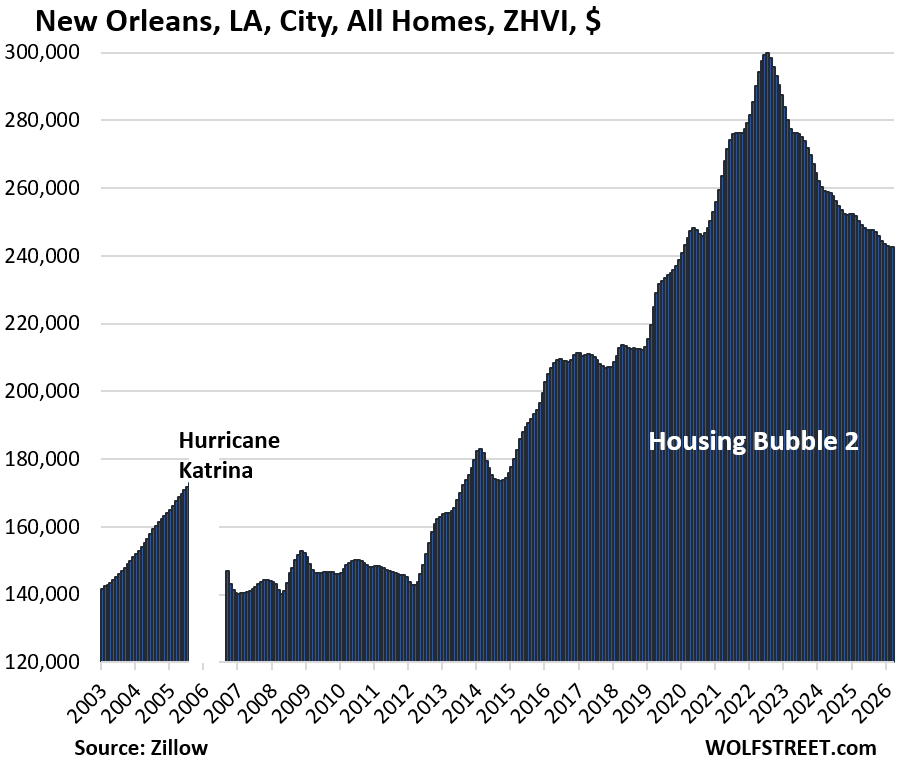

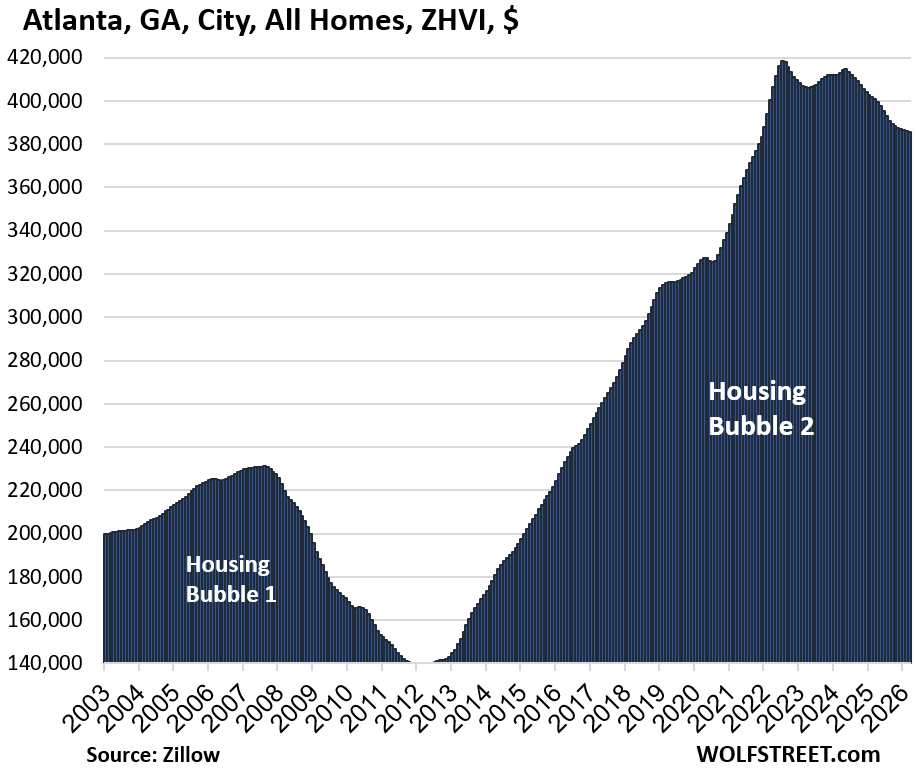

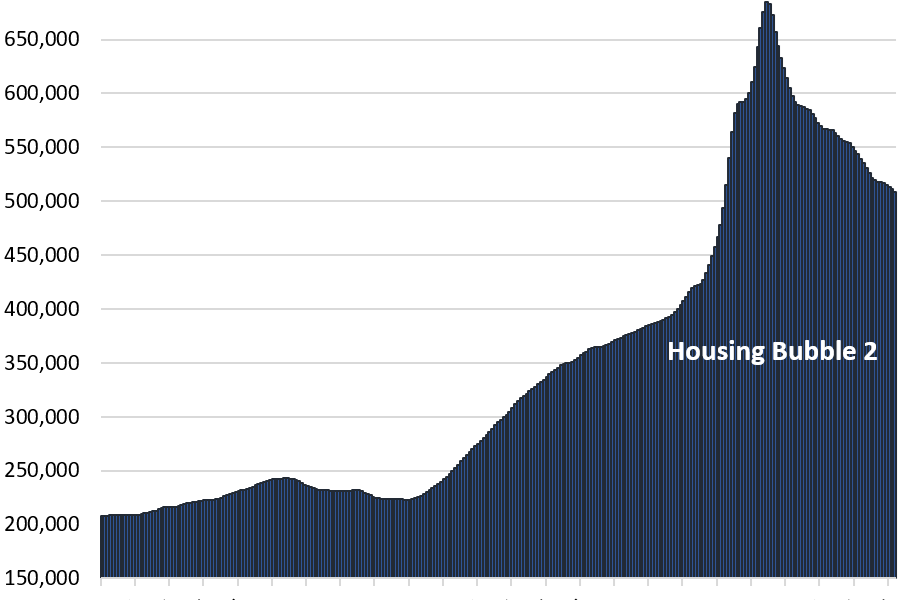

In March 2026, mid-tier home prices dropped from their peaks in 27 of 33 major, expensive US cities, according to Zillow’s Home Value Index (ZHVI). This index tracks the middle third of prices for single-family homes, condos, and co-ops, using a seasonally adjusted three-month average from millions of data points—including public records, MLS listings, and off-market deals. Austin saw the steepest fall at 26%, followed by Oakland at 25% and New Orleans at 19%. These declines signal a broad correction after years of frenzy.

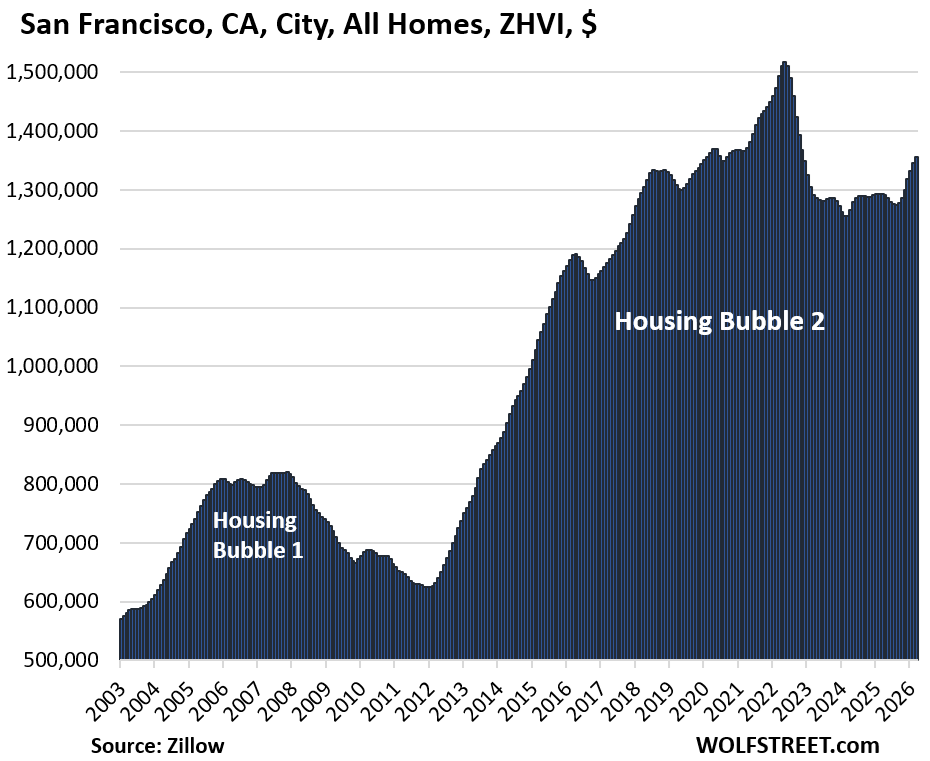

The outliers reveal regional fractures. San Francisco, ground zero for the AI investment surge, bucks the trend in mid-tier homes. A “mansion shortage” leaves ultra-high earners from firms like OpenAI and Anthropic short on luxury inventory. They spill over into mid-tier properties—typically $1.5-2.5 million there—driving a recent spike. Yet these prices remain 11% below the 2022 peak. Citywide, employment dipped, unemployment edged up to around 5%, and total jobs shrank by 2% year-over-year. San Jose, home to deeper tech pockets, saw mid-tier prices dip further; its median exceeds San Francisco’s at $1.8 million. Boston hovers in limbo: down 1% from April 2025’s record, but too tight to judge.

Cities Hitting New Highs—and the Tamer Pace

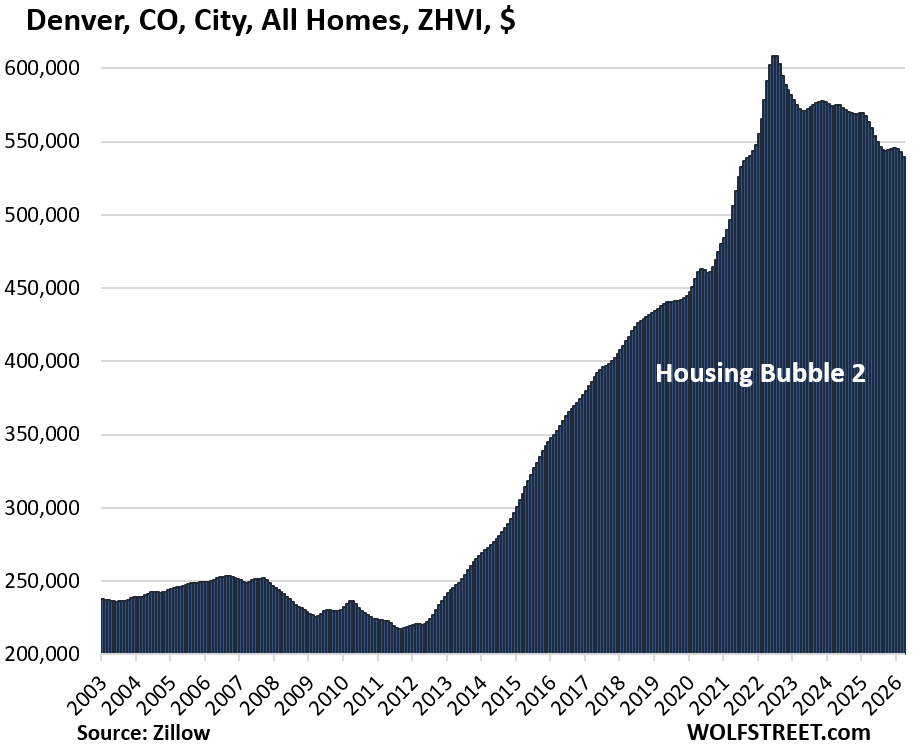

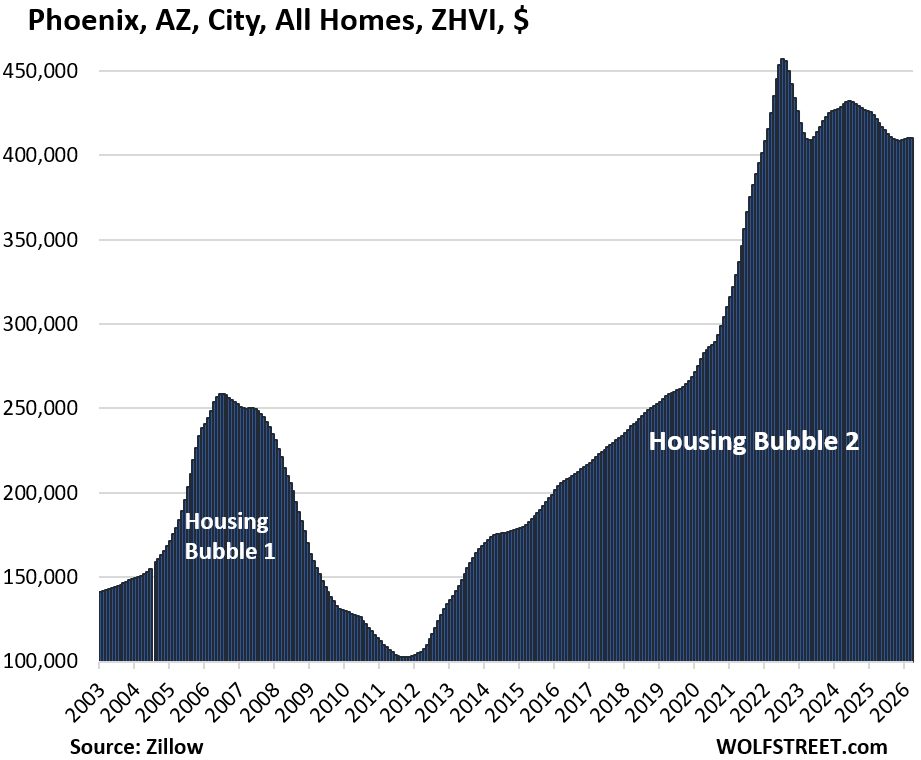

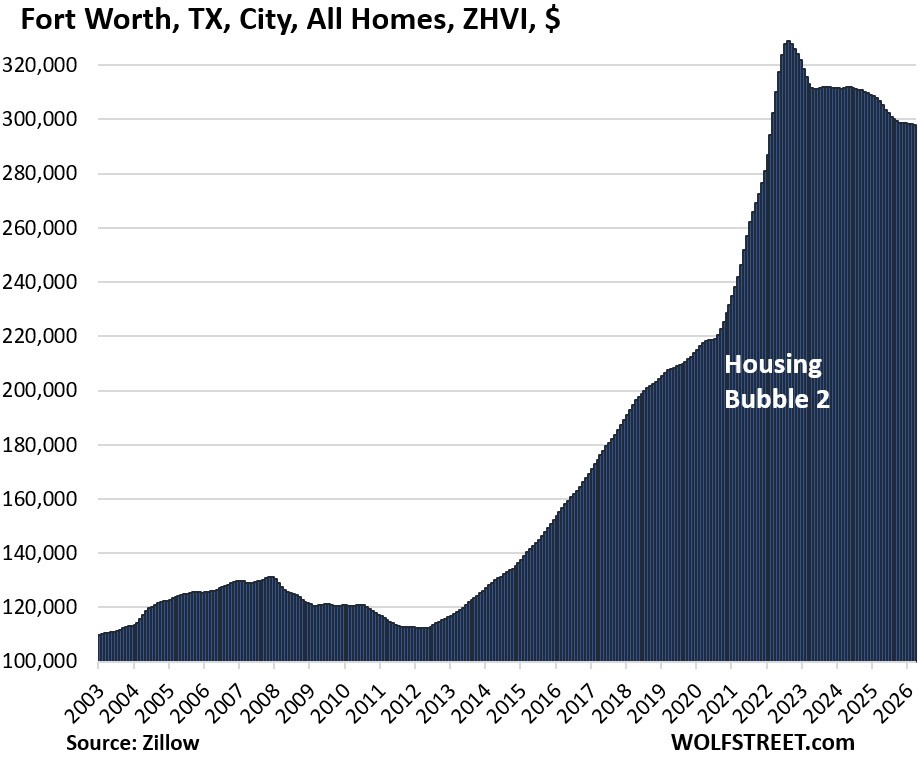

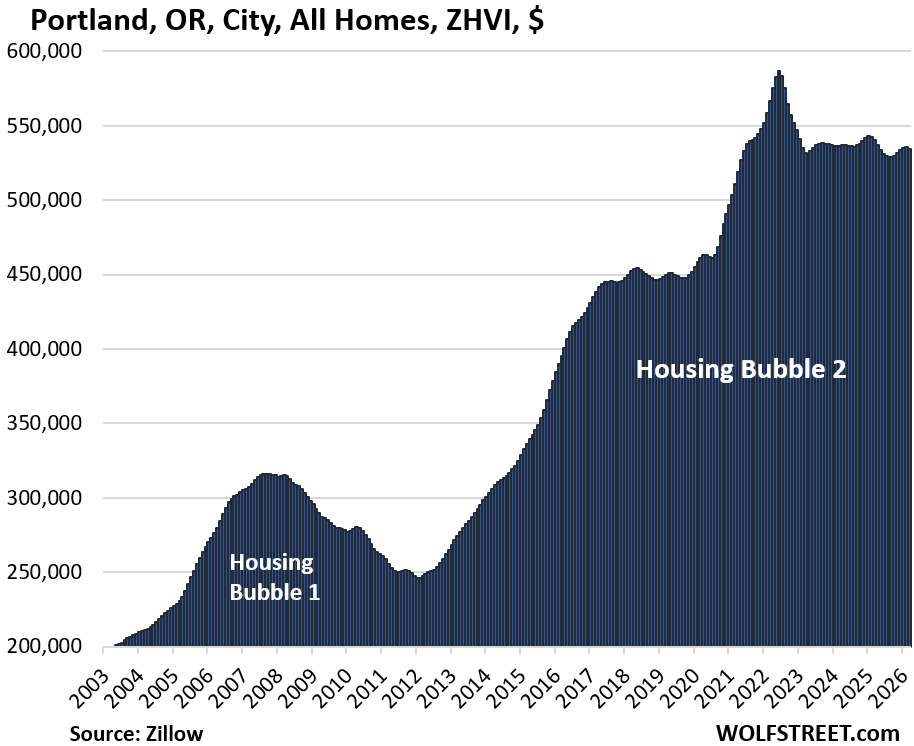

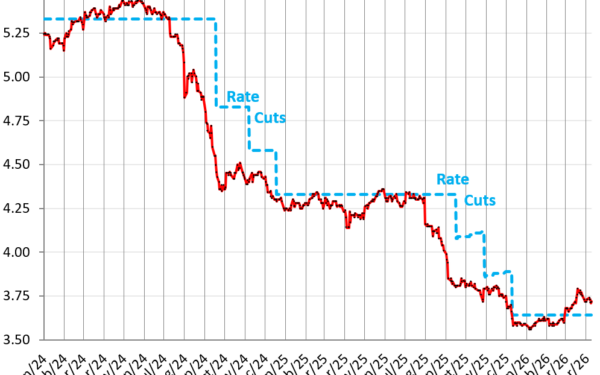

Five cities reached fresh ZHVI highs in March 2026: New York City, Chicago, Philadelphia, Minneapolis, and Omaha. Gains look modest compared to the 2021-2022 blowout. Back then, Austin rocketed 62%, Phoenix 60%, Fort Worth 50%, Raleigh 49%, and Sacramento 39%—all in two years. Those surges rode the Fed’s $5 trillion balance sheet expansion, buying Treasuries and mortgage-backed securities. Mortgage rates plunged below 3% even as CPI inflation hit 9.1% in June 2022. FOMO fueled bidding wars; homes sold 20-30% over ask in hot spots.

Today, rates linger near 7%, locking in 80% of owners with sub-5% loans. Inventory rose 20-30% year-over-year in many markets, per Redfin data, easing pressure. New highs in NYC (median mid-tier ~$800k) and Chicago (~$350k) reflect steady demand from finance and Midwest stability, not mania. Omaha’s inclusion underscores flyover resilience; its mid-tier ZHVI crossed $300k threshold years ago, qualifying for this “splendid bubbles” list of populous, pricey metros.

Why This Correction Matters Now

Housing drives 70% of US household wealth. Price drops erode that base, curbing consumer spending—already soft at 2.1% real growth in Q1 2026, per BEA estimates. Mid-tier focus matters because it captures working families, not just luxury flips. Austin’s plunge tracks tech layoffs: 15,000 jobs cut in Travis County since 2022 peaks, per state data. Remote work shifts favor cheaper Sun Belt satellites over coastal cores.

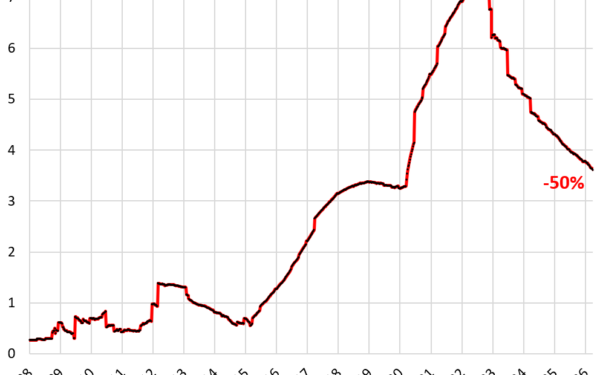

Skeptically, ZHVI isn’t repeat sales like Case-Shiller; it estimates values, potentially lagging market shifts. But Zillow’s database spans 110 million homes, making it robust. Inventory remains 40% below pre-pandemic norms nationally, per NAR, so rebounds loom if rates fall to 6%. AI’s $100 billion+ 2025 investments, per CB Insights, prop SF but risk bubble parallels to dot-com 2000, when Bay Area prices halved.

Implications ripple to finance: lower home equity squeezes HELOCs ($300 billion outstanding), once a spending engine. Crypto correlations? Housing cooled as Bitcoin stabilized post-2024 halving; both fledged Fed largesse. Investors eye munis and REITs for yield amid 4.5% Treasuries. For buyers, opportunity knocks in Austin (median now $480k vs. $650k peak). Sellers in cooling markets face longer days-on-market, up 25% nationally. Track April data; if declines deepen, recession odds rise to 35%, per NY Fed models. This isn’t collapse—it’s reality reasserting after excess.