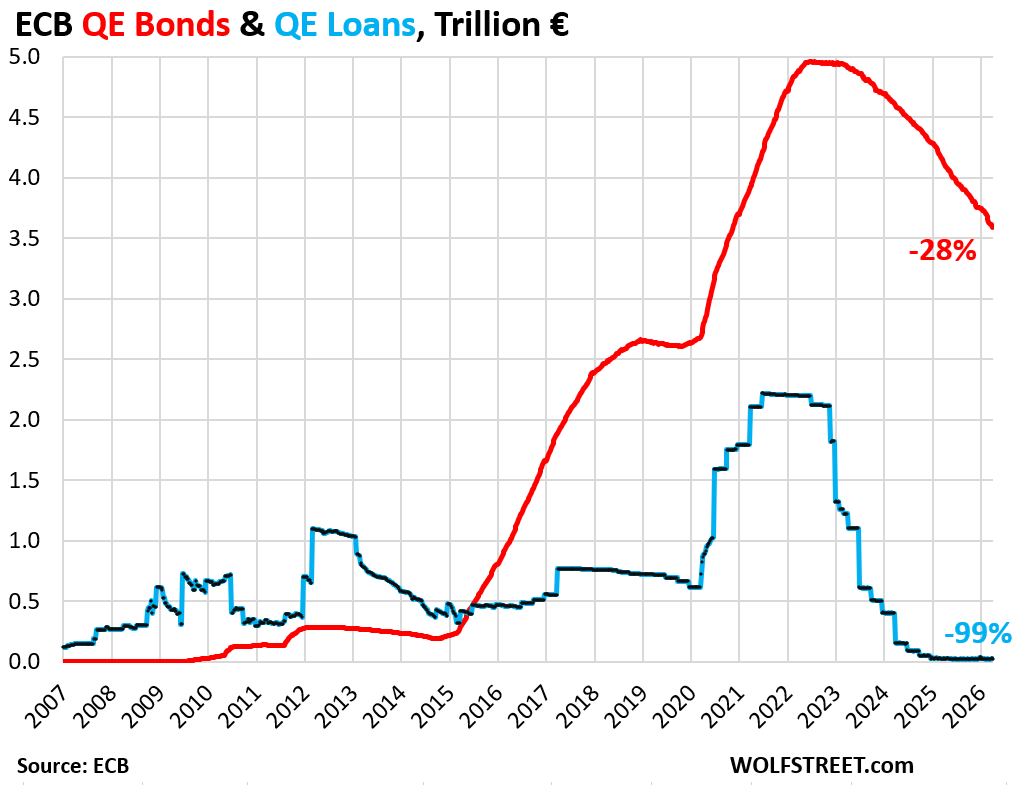

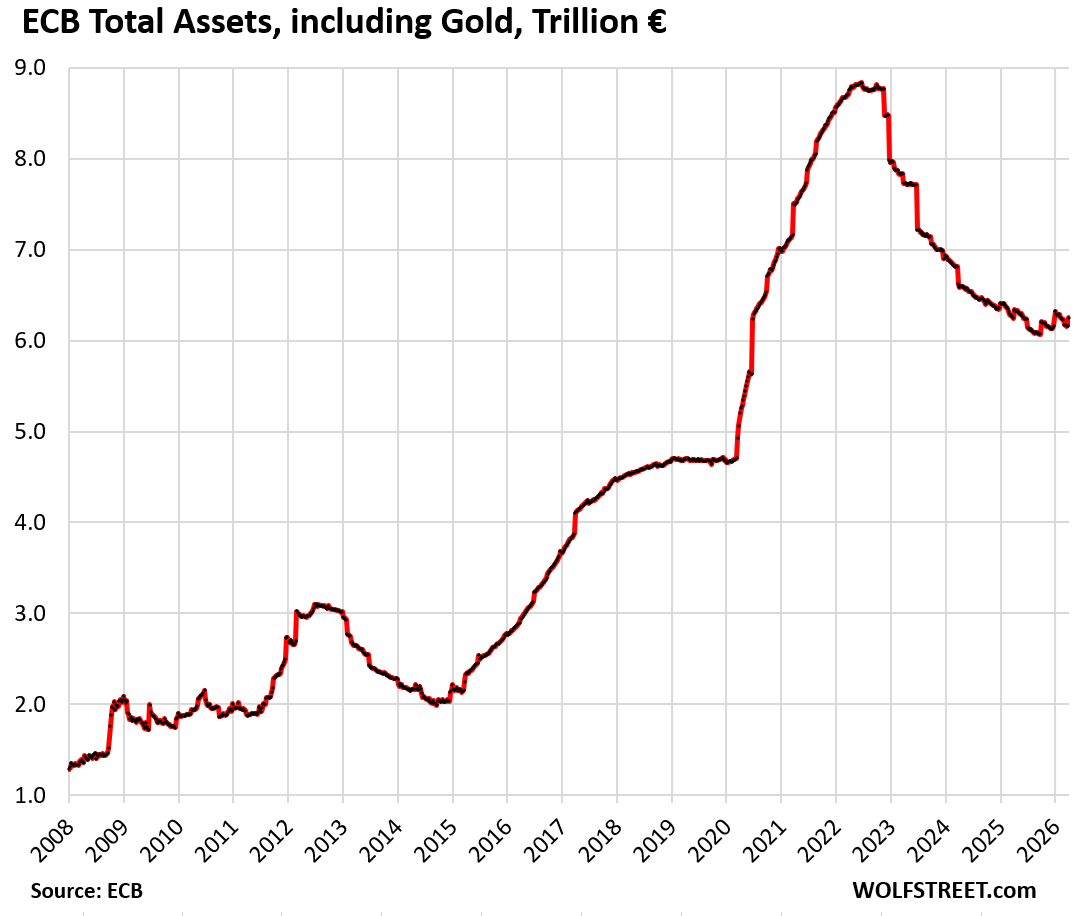

The European Central Bank (ECB) shed €66 billion in bonds and loans during March, pushing its quantitative tightening (QT) total to €3.55 trillion since mid-2022. That wipes out exactly 50% of its peak quantitative easing (QE) assets, which hit €7.16 trillion when inflation surged. No one expected this from the ECB, once labeled uber-dovish for its endless bond-buying sprees.

Break it down: QE bloated the ECB’s balance sheet through two channels—loans to banks and outright bond purchases. Loans peaked at €2.2 trillion; the ECB killed them off by 99% through unattractive repayment terms that banks rushed to escape. Bonds, mostly government debt from eurozone states plus some corporates and securitized assets, dropped 28% from €4.96 trillion to €3.59 trillion. These mature naturally now, with no reinvestments since early 2025 caps vanished. The ECB’s balance sheet today stands at €6.25 trillion after this month’s purge.

QT Mechanics and ECB’s Edge Over the Fed

The ECB runs a cleaner QT machine than the US Federal Reserve. It lets loans expire via bank repayments and bonds roll off at maturity—no forced sales that spike yields. Since July 2022, monthly caps limited reinvestments: €15 billion for public sector bonds from April 2023, plus proportional private sector cuts. Full uncapping in March 2025 accelerated the unwind. Contrast this with the Fed, which still replaces some maturing Treasuries and mortgages, shrinking its $7.2 trillion portfolio at a snail’s pace of $25-35 billion monthly.

Why does this matter? A bloated balance sheet locks central banks into low-rate traps. Unwinding prevents excess liquidity from fueling inflation when rates eventually drop. The ECB’s success—halving QE assets without market meltdowns—proves even “dovish” institutions can normalize aggressively. Eurozone bond markets absorbed the supply; 10-year Bund yields hover around 2.2%, stable despite €3.55 trillion in redemptions. Skeptics worried about liquidity crunches or periphery debt spikes, but so far, no cracks.

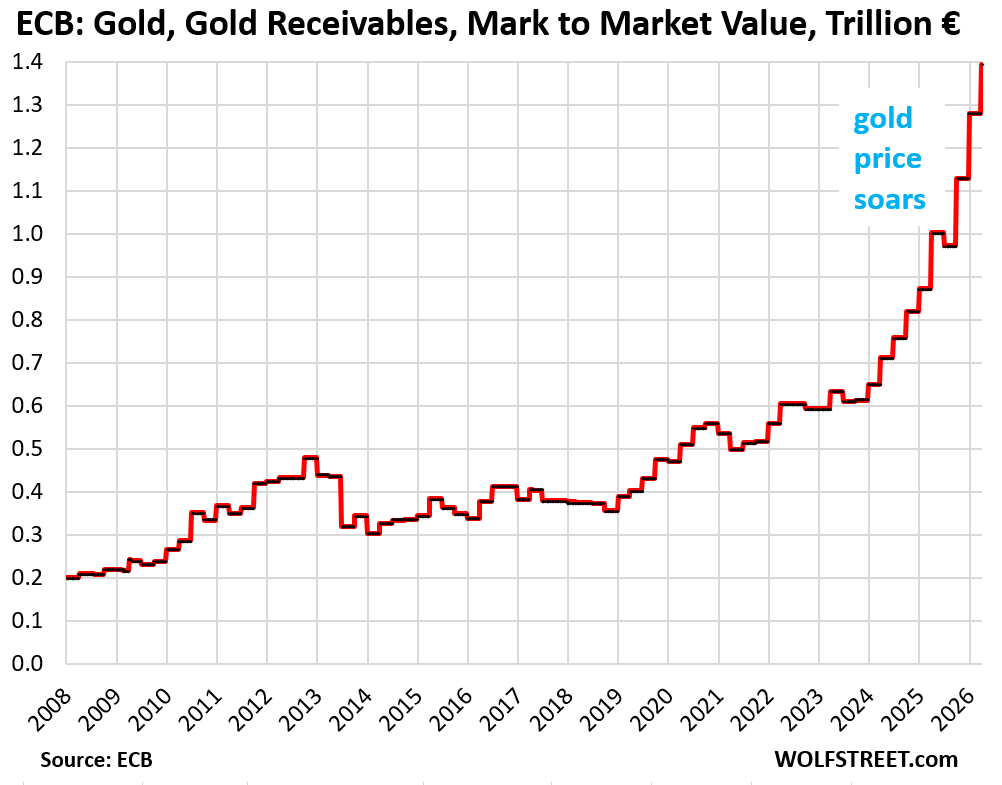

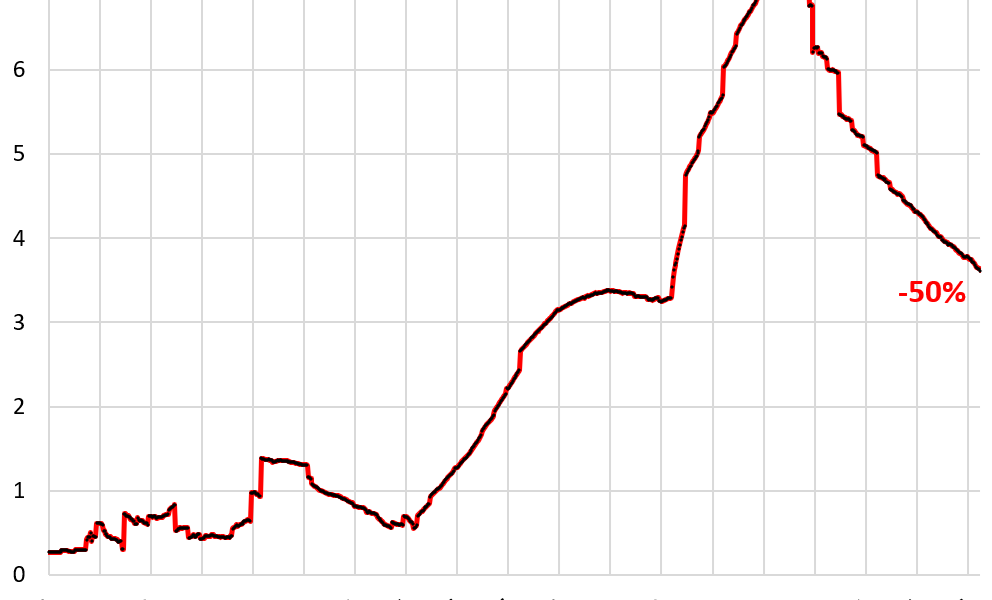

Gold Mark-to-Market Boosts Assets

Offsetting QT shrinkage, the ECB marked its gold holdings to market quarterly—unlike the Fed’s annual tweaks. Q1 saw a €113 billion uplift to €1.39 trillion, driven by gold’s euro price climb after January’s rally and February’s dip. Over five quarters, mark-ups totaled huge gains; since mid-2019, nearly €1 trillion in paper profits as gold surged from geopolitical tensions, de-dollarization bets, and central bank hoarding.

These are non-cash adjustments: no sales, no printing, just accounting reflecting end-quarter prices. Gold represents pooled holdings from 20 eurozone central banks, including Bundesbank’s 3,355 tonnes (largest chunk). Bulgaria’s 2026 euro entry will add its reserves next. Total assets rose €91 billion weekly to €6.25 trillion, masking QT progress visually but not fundamentally.

Implications cut deep into finance and security. Gold’s €1.39 trillion valuation—22% of ECB assets—hedges against fiat debasement and euro weakness. In a fragmenting world, with BRICS pushing de-dollarization and crypto as digital gold, the ECB’s transparency signals prudence. Yet skepticism lingers: mark-to-market swings could reverse if gold corrects 20-30% on rate hikes or risk-off flows. QT halves QE bloat, but €3.59 trillion in bonds remains a inflation time bomb if recession forces rate cuts and restarts QE.

Broaden the lens: ECB’s QT outpaces peers. Bank of England shed 25% of QE; Bank of Japan still expands. For investors, this means tighter euro liquidity—watch bank lending squeeze and money market rates. Eurozone growth stagnates at 0.3% quarterly; QT aids disinflation (CPI at 2.4%) but risks tipping into deflation. Crypto holders note: ECB gold gains mirror Bitcoin’s 2024 surge, underscoring hard assets’ appeal amid fiat experiments. The ECB delivers where others falter—50% unwind proves central banks can shrink without apocalypse. But markets bet on policy U-turns; stay vigilant.