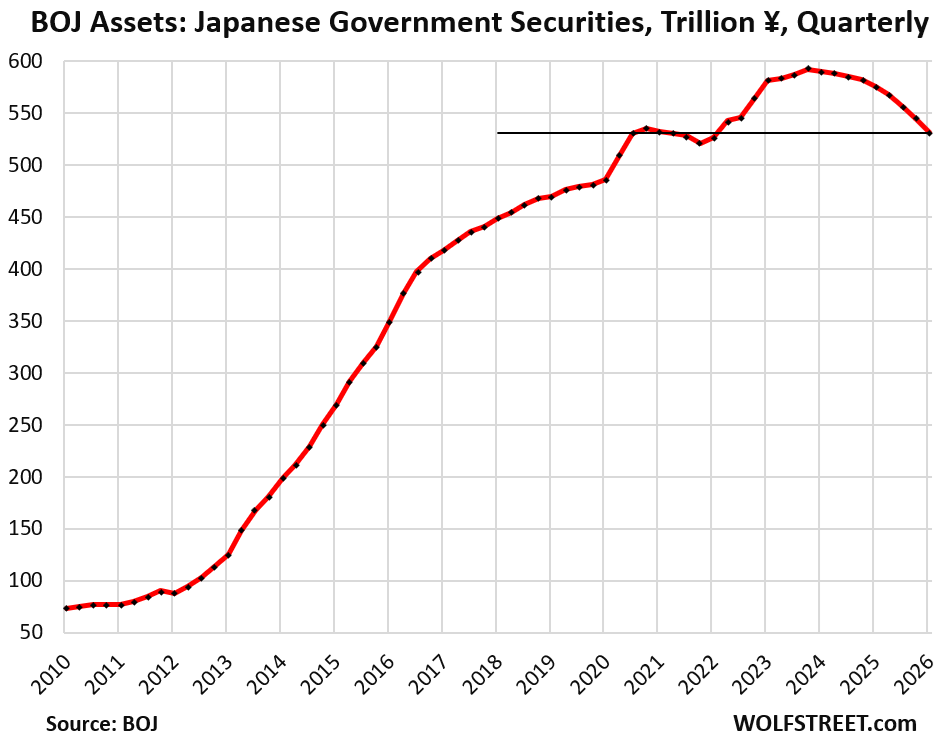

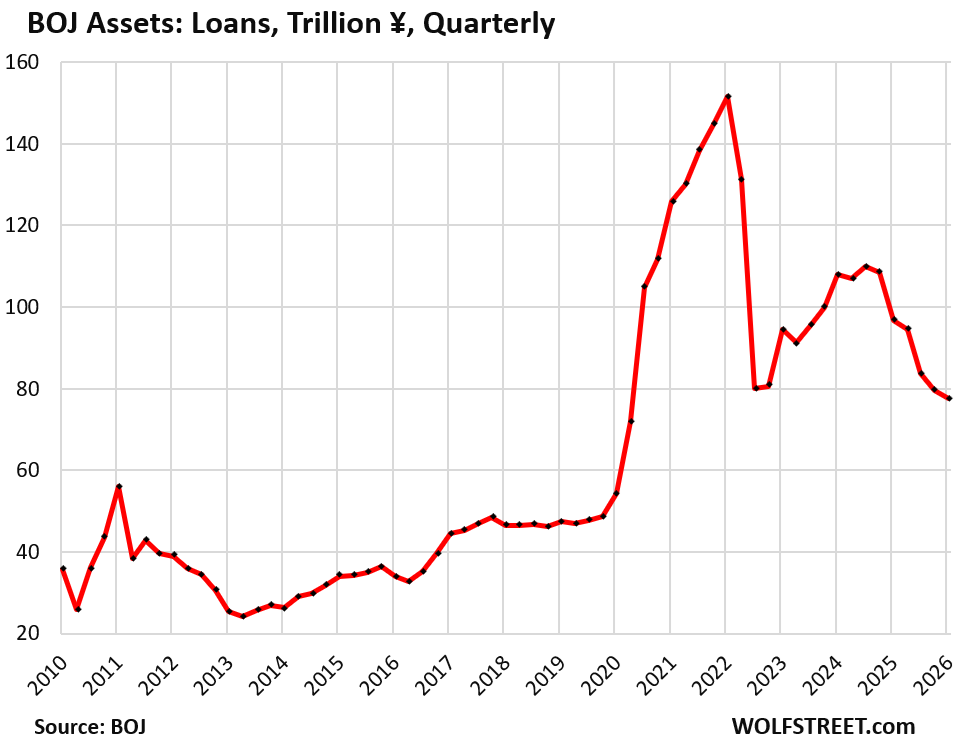

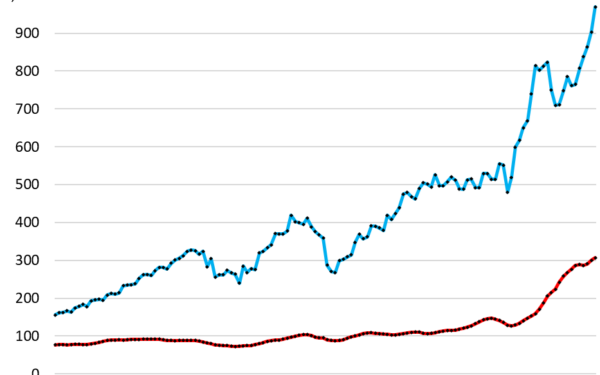

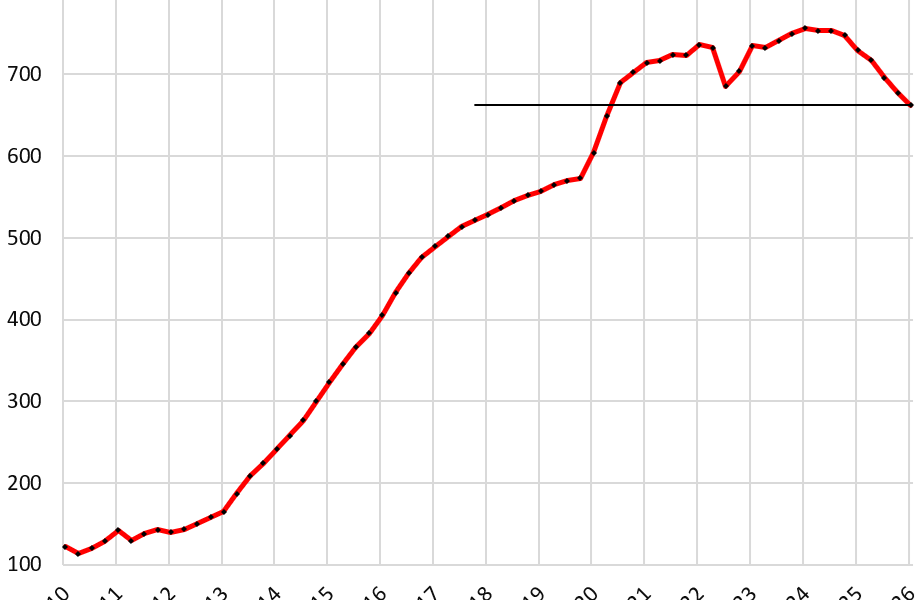

Bank of Japan slashed its balance sheet by 12.6% from its peak, accelerated quantitative tightening (QT), and kicked off sales of equity ETFs and J-REITs. This marks a sharp pivot from years of money-printing that bloated its assets to over ¥770 trillion by late 2023. The central bank now holds about ¥670 trillion, shedding roughly ¥100 trillion mainly through letting Japanese Government Bonds (JGBs) mature without full reinvestment.

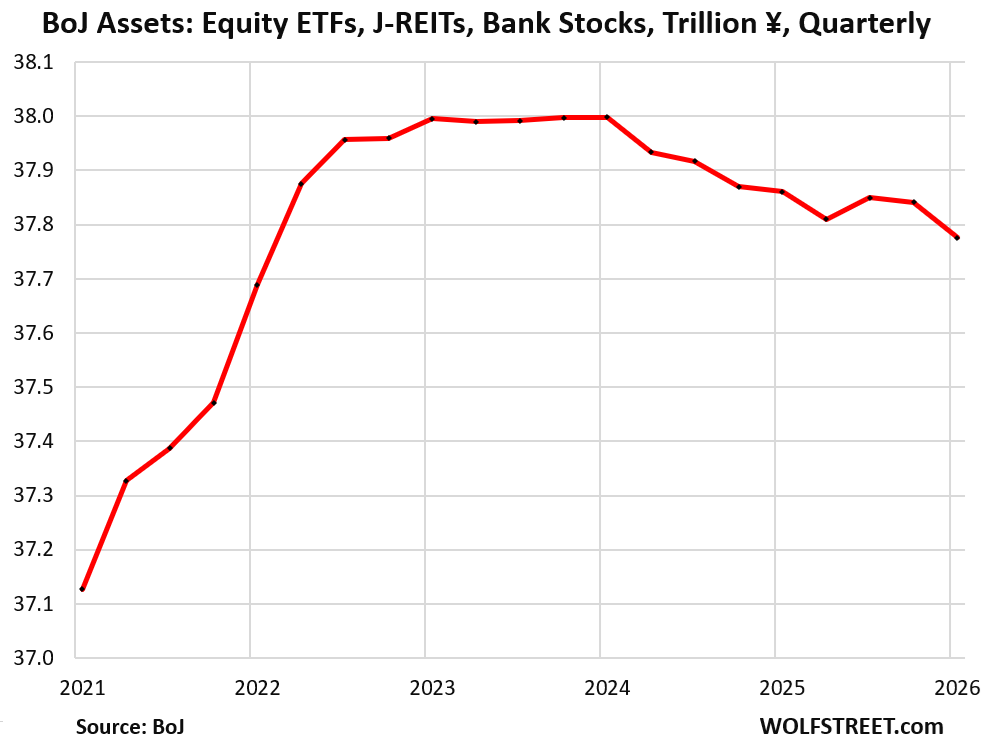

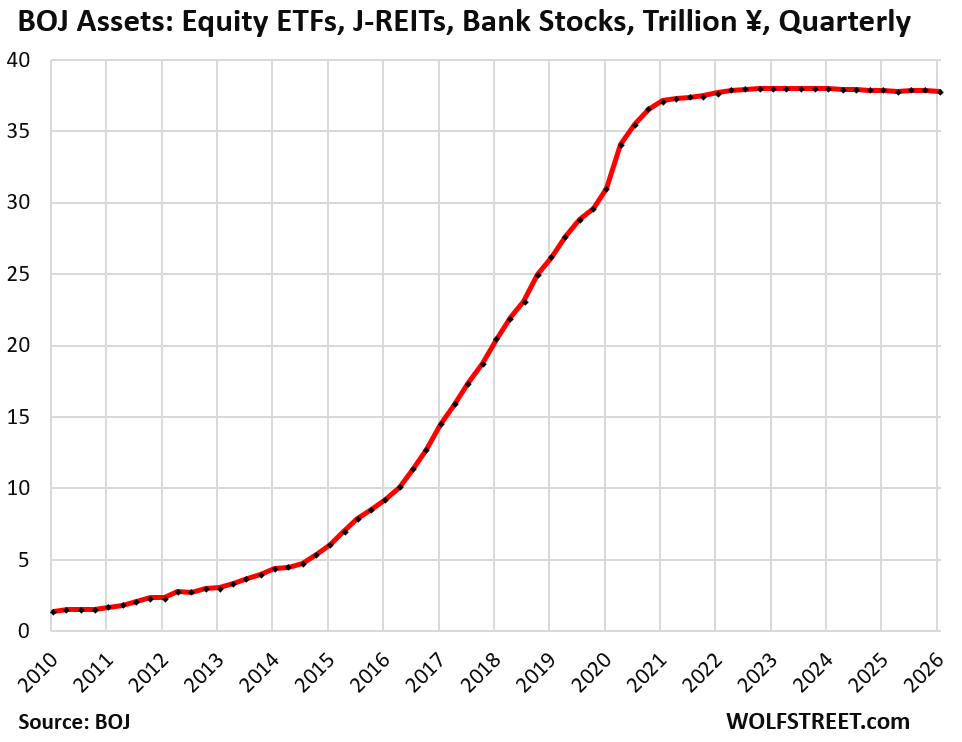

BOJ announced these moves in its July 2024 policy meeting. It halved planned JGB purchases to ¥3 trillion per month starting next fiscal year, down from ¥6 trillion. For riskier assets, BOJ will sell equity ETFs—valued at ¥37 trillion—and J-REITs worth ¥2.5 trillion—once stock markets stabilize. Sales start small: up to ¥500 billion in ETFs and ¥100 billion in REITs annually. This reverses a decade of the bank becoming Japan’s largest equity holder, with stakes in over 80% of TOPIX companies.

Why QT Now, Not Rate Hikes

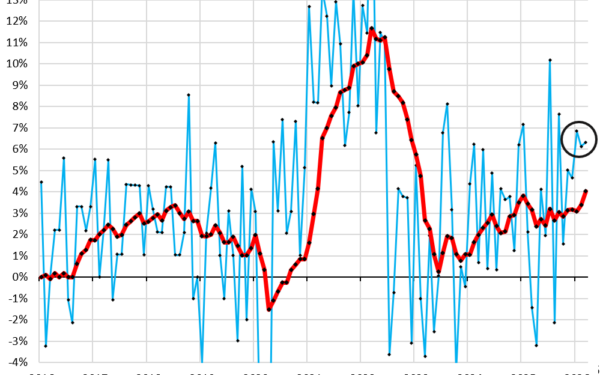

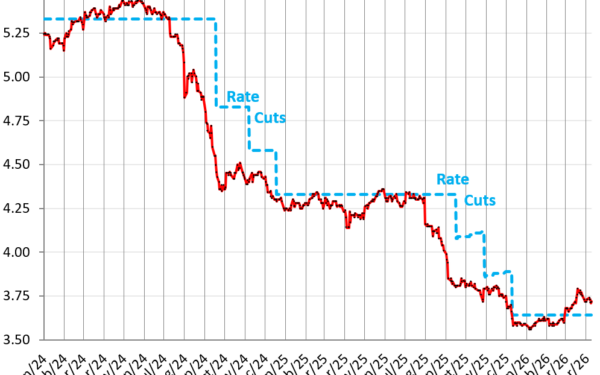

BOJ targets a floor under the yen—trading near 150 to the dollar—and caps inflation without aggressive rate hikes. Core CPI hit 2.8% in July 2024, above the 2% goal for 28 straight months, but wage growth lags at 2.5%. Hiking rates to 0.5% or more risks fracturing the JGB market, where yields spiked to 1.1% on 10-year bonds post-July’s 0.25% hike. QT drains liquidity quietly, mopping up excess yen chasing higher US yields.

Yen weakness stems from interest rate differentials: US fed funds at 5.25-5.50% versus BOJ’s near-zero until recently. Carry trades amplified this—investors borrowed cheap yen to buy US assets. BOJ’s QT signals policy normalization, potentially strengthening the yen by reducing supply. Yet skeptics doubt its punch: past tapers barely dented the balance sheet until now.

Market Ripples and Risks

Japanese stocks tanked 12% on August 5, 2024—the worst single-day drop since 1987—after BOJ’s hike and QT hints unwound carry trades. Nikkei recovered somewhat but volatility lingers. BOJ’s ETF sales could pressure equities further; it already dumped ¥10 trillion in holdings during 2020-2022 volatility. J-REITs face headwinds from rising yields squeezing property values.

Globally, this matters because BOJ owns 50% of JGBs outstanding, propping up fiscal deficits averaging 6% of GDP. Shrinking the balance sheet tests market absorption: private buyers must step up or yields surge, hiking Japan’s ¥1,300 trillion debt service costs. Success here could embolden other central banks—Fed, ECB—to exit QE without chaos.

But risks loom. Abrupt QT might trigger liquidity crunches, echoing 2022 UK gilt crisis. BOJ paused sales during COVID and 2022 inflation spikes, prioritizing stability. Current path seems measured—12.6% cut over 18 months averages ¥5 trillion monthly runoff. If yen rebounds to 140/dollar and inflation eases, BOJ exits the “bazooka” era. Failure invites more hikes, market turmoil, or yen freefall past 160.

Investors watch JGB auctions and ETF flows closely. BOJ’s next meeting in September 2024 could tweak pace based on data. This isn’t hype-driven normalization; it’s a calculated unwind of distortions built since Abenomics 2013. Japan’s experiment tests if giants can shrink without collapsing.