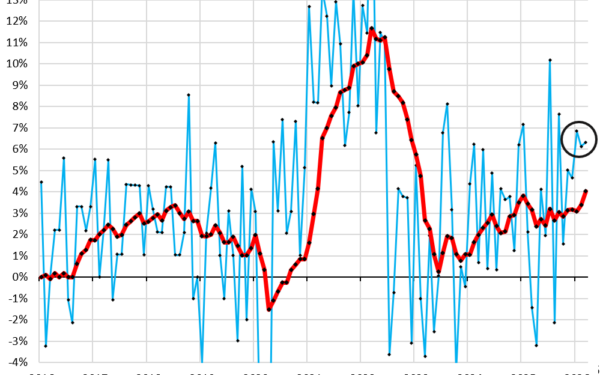

US manufacturers received durable goods orders totaling $315 billion in February, down 1.4% from January but up 7.3% from a year earlier. Strip out the noise from Boeing’s erratic jet orders and defense spending, and the picture sharpens: core orders excluding aircraft and defense hit a record $278 billion, up 1.5% month-over-month and 5.8% year-over-year. This 12-month average trend—+8.8% year-over-year—confirms manufacturing demand is accelerating after years of stagnation.

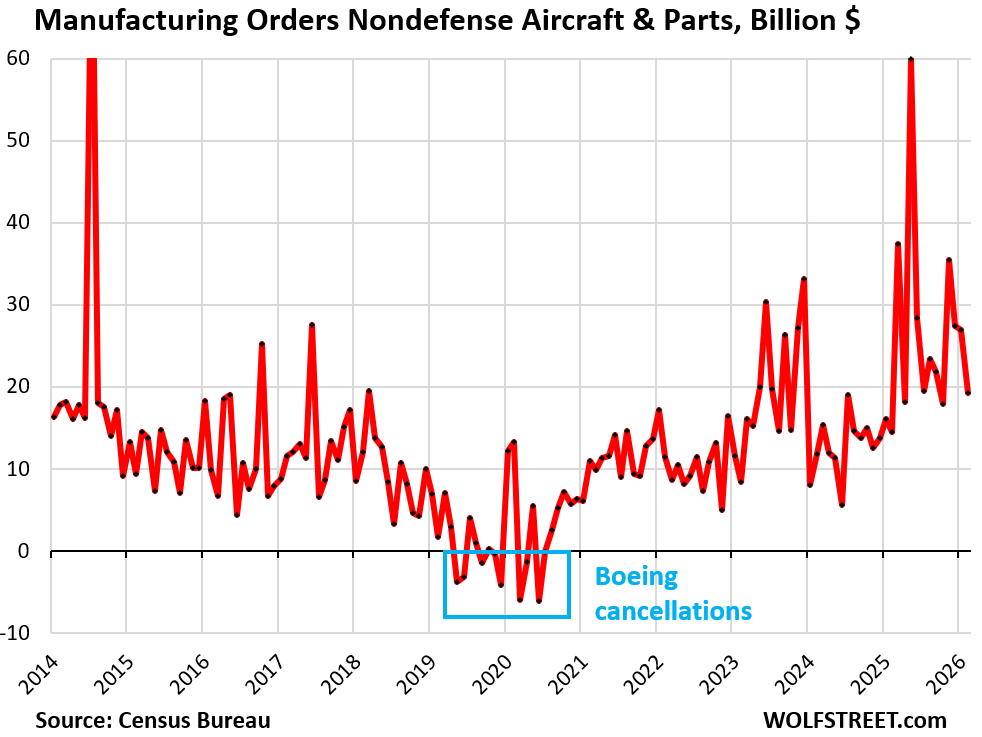

Why fixate on these adjusted figures? Raw data swings wildly due to lumpy aircraft deals. Boeing snagged massive orders in some months—think 30 jets worth billions—then nothing the next. February saw nondefense aircraft orders drop 7.7% to $19.2 billion from January, yet still 33% above last year. Defense adds more unpredictability amid ongoing conflicts. Ignore them, and you see steady underlying strength. These orders signal capital spending intentions, a leading indicator for industrial output, jobs, and GDP. Manufacturing drives just 11% of US GDP but anchors supply chains and national security.

What’s Driving the Gains

Six of seven major categories posted month-over-month increases. Computers and electronic products led with +4.9% to $28 billion, fueled by AI data center builds and semiconductor reshoring. Motor vehicles and parts rose 3.1% to $71 billion, boosted by EV production ramps despite softening demand. Primary metals climbed 2.2% to $29 billion, machinery 1.5% to $41 billion, fabricated metals 0.5% to $43 billion, and other durables 0.5% to $50 billion. Only electrical equipment dipped slightly (-0.1% to $18 billion), but it’s up 6.4% year-to-date.

Context matters: post-pandemic, orders flatlined through 2024 after a 2021-2022 surge. Now, early 2025 marks a breakout. Semiconductor orders reflect CHIPS Act subsidies—$52 billion in grants and loans disbursed to firms like Intel ($8.5B) and TSMC ($6.6B) for US fabs. Auto gains tie to Inflation Reduction Act tax credits pushing $100B+ into EV batteries and plants. These aren’t organic booms; policy juices them. Skeptically, grants risk taxpayer losses if projects flop—Boeing’s woes remind us execution falters. Tariffs under Trump 1.0 added 25% on steel, nudging some reshoring but hiking costs passed to consumers.

Implications for Economy and Policy

This matters because it challenges the “deindustrialization” narrative. Reshoring reduces reliance on China for critical tech—semiconductors power everything from missiles to iPhones. Biden’s industrial policy mirrors Trump’s but scales up: IRA pours $369B into clean energy, CHIPS targets 20% global chip market share by 2030. Results show in orders, but jobs lag—automation eats gains, and new fabs employ few relative to subsidies.

Broader economy: rising capex supports productivity, potentially curbing inflation without recession. Fed watches this; durable goods up 8.8% YoY bolsters soft-landing bets, keeping rates steady. Risks loom—consumer spending slowdown could hit autos, geopolitical flares spike defense volatility. Boeing’s order book, bloated at 5,600 planes yet delivery-starved by strikes and quality issues, distorts less here but underscores fragility.

Bottom line: US manufacturing orders signal resilience and policy payoff, but volatility persists. Watch core trends—they predict output better than headlines. If sustained, expect factory hiring and supply chain shifts; if not, subsidies wasted. Data from Census Bureau; track ISM PMI for confirmation.