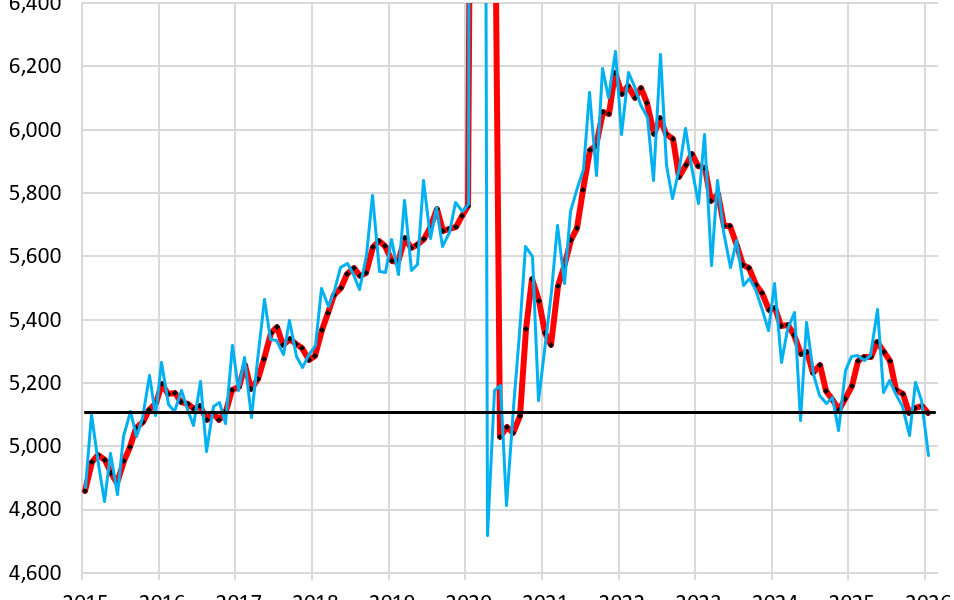

US labor market separations dropped to 4.97 million in February, the lowest level since 2015 outside the 2020 lockdown months. This figure, from the Bureau of Labor Statistics’ Job Openings and Labor Turnover Survey (JOLTS) covering 21,000 business locations, signals unusually low churn. Fewer people quit, get fired, retire, or leave for other reasons means fewer job openings and hires overall.

The three-month average separations fell to 5.11 million, also a post-2015 low excluding lockdowns. Compare this to pre-pandemic norms: separations hovered around 5.5-6 million monthly from 2016-2019 as employment grew by over 10 million jobs. Now, with employment near 158 million, this stasis locks workers in place, creating an employer-friendly equilibrium.

Breakdown of Separations

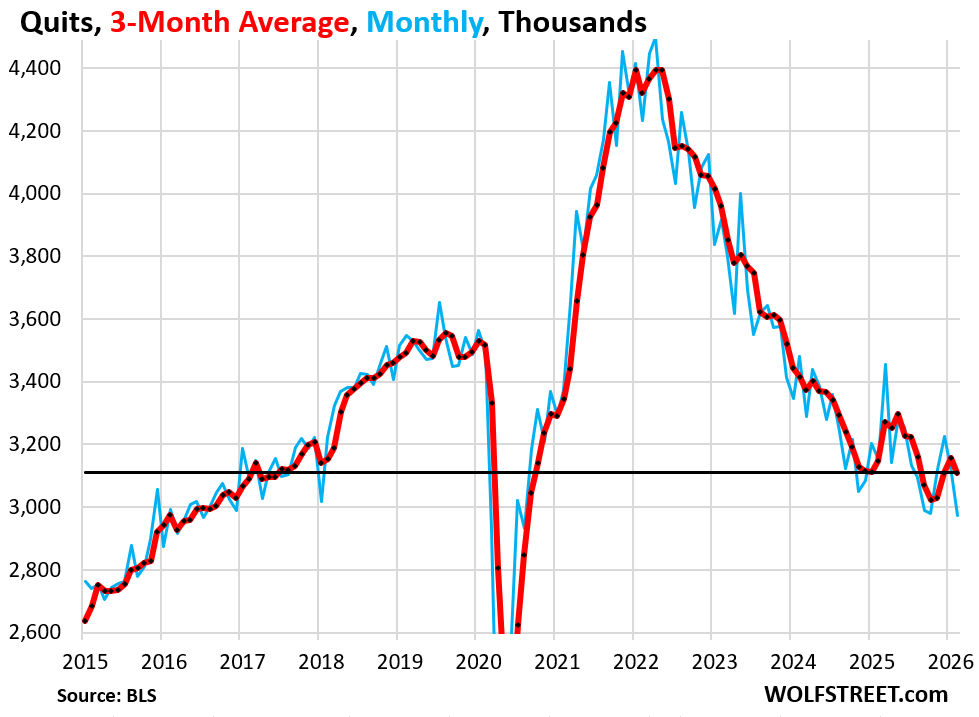

Voluntary quits, which make up 60% of separations, plunged to 2.97 million—the lowest since 2017-2018 outside lockdowns. The three-month average hit 3.11 million. Quits drive market dynamism: workers jumping for better pay or roles create openings that fuel hiring. When quits stall, the pipeline dries up.

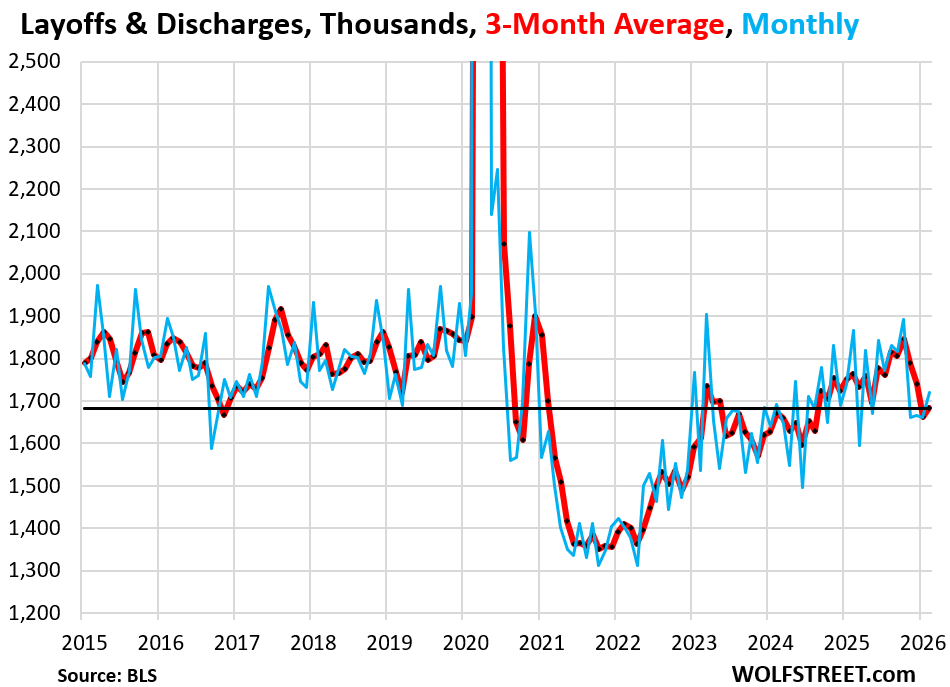

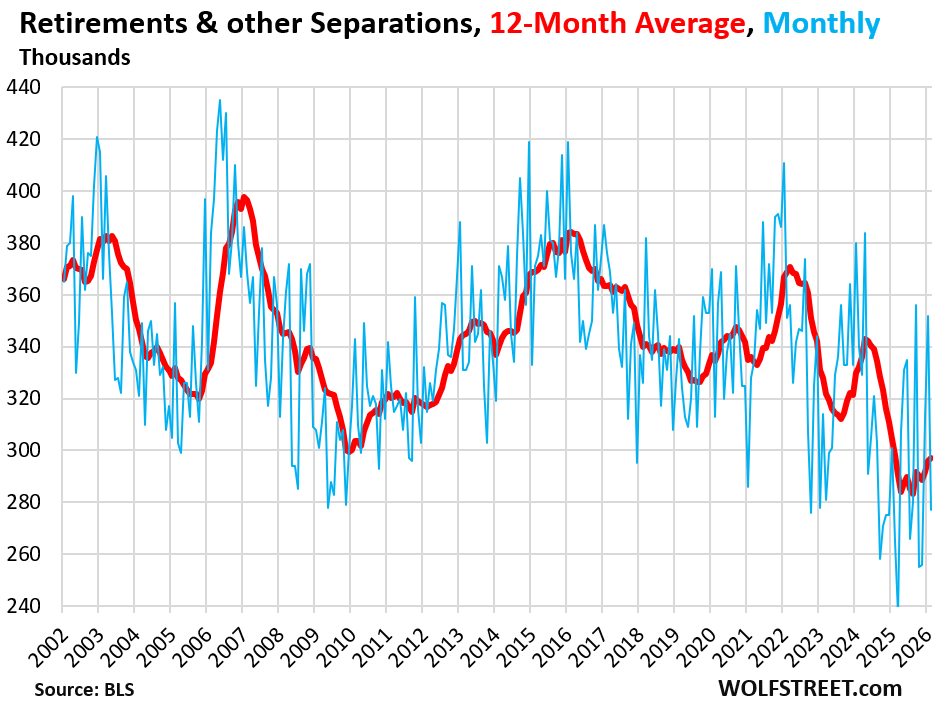

Layoffs and discharges rose slightly to 1.71 million, with a three-month average of 1.68 million—still below pre-pandemic peaks but higher than during peak labor shortages in 2021-2022. Retirements and other separations remain minimal at around 6% of total.

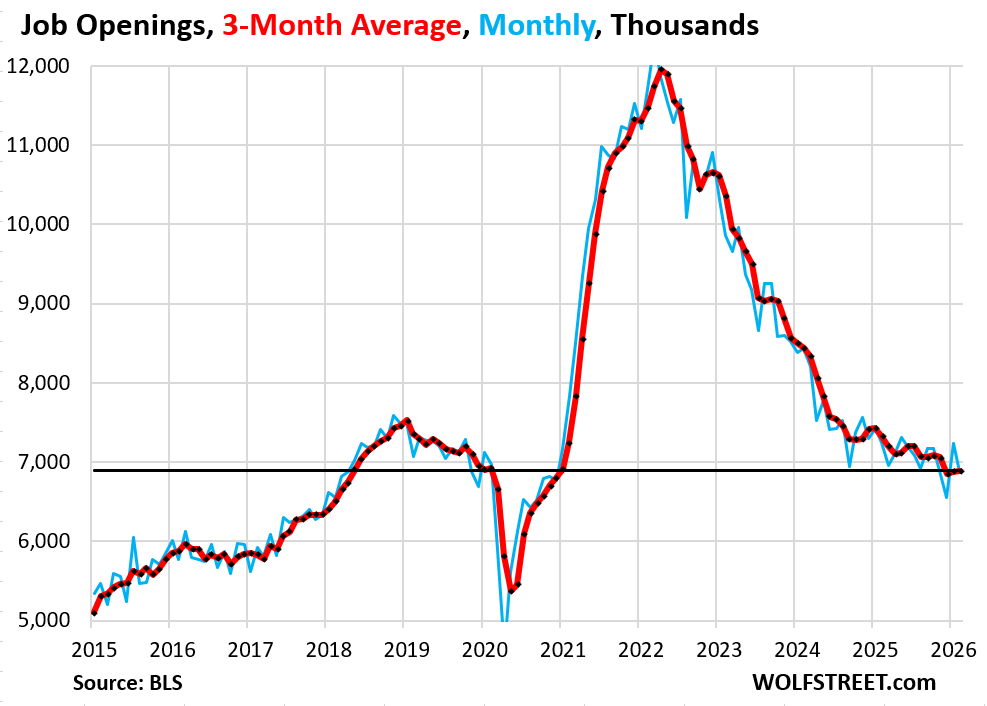

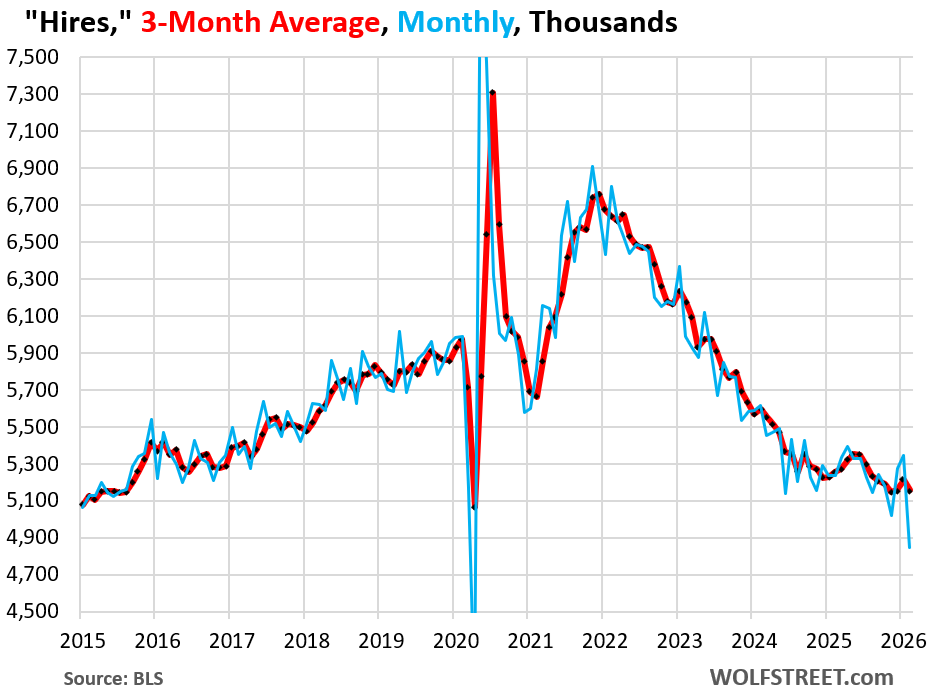

Job openings followed suit, dropping amid this low turnover. February’s 8.75 million openings (revised down) yielded a 5.1% rate on 171.8 million jobs—elevated but cooling from 2022 highs above 11 million. Hires ticked down too, reinforcing the slowdown.

Drivers Behind the Stasis

Tighter immigration controls play a role. Crackdowns on illegal entries and stricter work visas have shrunk labor supply by an estimated 1-2 million potential workers annually since 2023, per migration data from DHS and CBP. This exacerbates shortages in construction, hospitality, and agriculture, where foreign-born workers fill 25-30% of roles.

But don’t overstate it: quits were already trending down before immigration shifts. Broader caution grips workers—high interest rates, cooling consumer spending, and tech layoffs have raised job-security fears. The quit rate sits at 1.9% of employment, half the 2022 peak and below the long-term 2.2% average.

Employers contribute too. Many hoard labor rather than risk shortages, especially with training costs averaging $1,200-$2,000 per hire in tight markets. Wage growth has slowed to 4% year-over-year, per BLS, removing the “jump ship for more money” incentive.

Why This Matters

This peculiar calm favors incumbents: stable staffing cuts turnover costs (estimated at 20-50% of salary per employee) and boosts short-term productivity. But it harms market efficiency. Low mobility mismatches skills—think overqualified baristas or understaffed factories.

Young workers suffer most. Entry-level openings rely on quits from mid-career roles; with fewer, unemployment for 16-24-year-olds lingers at 12-13%, double the overall 3.9% rate. Lifetime earnings take a hit: each year of delayed good-job entry costs 3-5% in wages, per Federal Reserve studies.

For the Fed, it’s a yellow flag. Low churn supports soft-landing hopes—no mass layoffs—but persistent tightness could reignite inflation if demand rebounds. Policymakers watch quits closely as a forward indicator; their drop preceded 2001 and 2008 slowdowns by months.

Skeptically, this isn’t collapse—unemployment stays low, participation edges up to 62.7%. Yet prolonged stasis risks stagnation. If immigration eases or rates fall further, churn could revive. Until then, the US labor market freezes in an uneasy balance: good for those inside, tough for outsiders.