Surging DRAM prices are slashing margins for makers of low-cost single-board computers (SBCs), threatening the hobbyist market that relies on boards like the Raspberry Pi. Spot prices for DDR4 chips jumped 13-18% in Q2 2024, per TrendForce data, with Q3 forecasts at another 8-13% hike. This stems from explosive AI demand sucking up high-bandwidth memory (HBM), spilling over into standard DDR4 and DDR5 supplies. For SBC vendors targeting $10-80 price points, RAM costs—often 20-30% of bill of materials—now devour profits, forcing production cuts or price hikes.

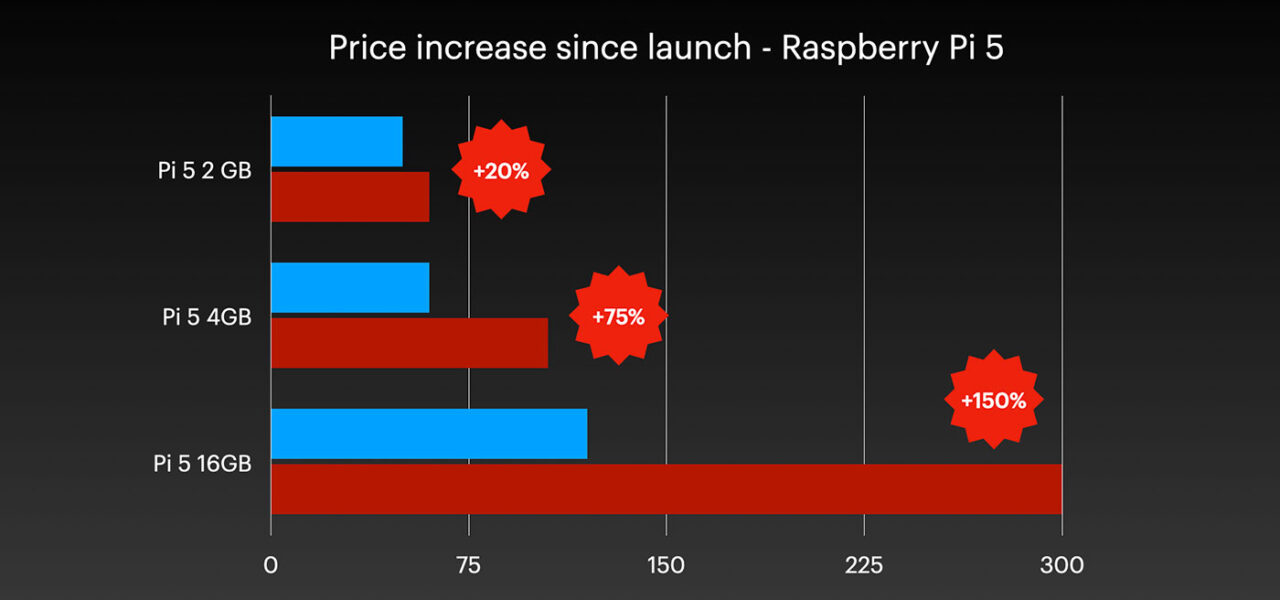

Raspberry Pi exemplifies the pain. The Pi 5, launched October 2023, lists a 4GB model at $60 and 8GB at $80. Estimates peg its BOM at $45-50, with 4-8GB LPDDR4X eating $10-20 alone. Foundation CEO Eben Upton confirmed in May 2024 earnings that component shortages, led by memory, capped output at 20,000-30,000 units weekly—half target capacity. They idled Pi 4 lines to prioritize Pi 5, but even Zero 2 W production stalled since late 2023. Broadcom’s EOL notice for Pi 4’s BCM2711 SoC adds pressure, but memory remains the bottleneck.

Broader SBC Market Squeeze

Competitors face identical headwinds. Banana Pi, Radxa, and Orange Pi—all Chinese firms pumping out Pi clones—report stockouts and 20-50% price bumps on 4GB boards. AliExpress listings for RK3588-based SBCs, once $50-70, now hover at $90+. Makers pivot to higher-margin industrial boards ($150+) or cut low-end SKUs. A June 2024 Digi-Key report shows SBC inventory down 40% year-over-year, with lead times stretching 20-30 weeks for LPDDR4X modules.

Supply chains expose the fragility. Top DRAM makers—Samsung, SK Hynix, Micron—allocate 60-70% capacity to AI servers and smartphones, per Counterpoint Research. HBM prices soared 200% in 2023-2024, bidding up contract prices for consumer DRAM by 30-50%. Geopolitical tensions, like US export curbs on China, further constrict flows. SBCs, with volumes dwarfed by billions of phone chips yearly, rank low on priority lists.

Why This Crushes Hobbyists and What Comes Next

Hobbyists lose cheap entry points for IoT, robotics, and learning projects. A Pi Zero at $5-10 fueled millions of deployments; replacements like ESP32 boards ($5) lack Linux horsepower. Makerspaces and schools budget $20-50 per student—$80 Pi 5s strain that. Used market booms on eBay, with Pi 4s fetching 1.5x MSRP, but supply dries up.

Implications ripple wide. Expect SBC makers to chase enterprise: Raspberry Pi’s industrial Pi 5 Compute Module hits $100+, with 70% margins vs. consumer’s 30%. Chinese firms undercut via gray-market chips, but quality dips—fake RAM plagues forums. Hobbyists shift to alternatives: Rockchip RK3566 boards ($40-60), Qualcomm Snapdragon dev kits ($200+), or x86 mini-PCs like Beelink ($150, full Windows). MCUs gain: ESP32-S3 or RP2040 for sub-$10 Linux-light tasks.

Skeptically, this isn’t terminal. DRAM cycles peak every 2-3 years; prices may dip by Q1 2025 as AI hype cools and fabs ramp. Raspberry Pi’s $240M revenue (FY2024) and Nvidia/ARM ties buffer them—Upton eyes 1M Pi 5/month by year-end. Yet prolonged pain accelerates fragmentation: premium SBCs for pros, dirt-cheap MCUs for tinkers. Why it matters? SBCs democratized computing since 2012’s Pi 1. Killing affordability hands reins to Big Tech boards, stifling grassroots innovation. Watch Q4 earnings for pivot signals.